Turkish Lira under dollar pressure

MUSTAFA SÖNMEZ - mustafasnmz@hotmail.com

It is expected that the dollar exchange rate, which has had a monthly average of 2.28 lira in December, will continuously climb in the following months of 2015. REUTERS Photo

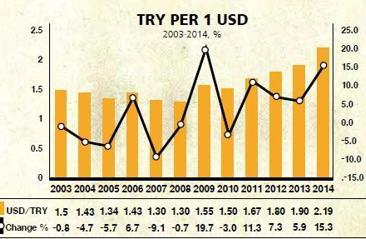

The year 2014 has been one in which the Turkish Lira plummeted under heavy pressure from the U.S. dollar. The lira last saw such pressure in 2009, the year when the global crisis took hold of Turkey. After overcoming that crisis, it again experienced the stress created by the climbing dollar in 2014. The lira is entering the new year with a lot of accumulated stress.

With only two work days left before 2015 arrives, if there are no shocking climbs in the lira value of the dollar, then the greenback will close December at an average of 2.28 liras and 2014 at an average of 2.19 liras. Thus, the lira will end the year 2014 with a value loss of 15.3 percent against the dollar. The dollar/lira parity closed 2013 with a loss of around 6 percent and an average of 1.90 liras. In 2014, it has experienced the sharpest devaluation since 2009.

After 2009 In 2009 when foreign investors withdrew immediately due to the harsh effect of the global crisis, the lira lost 19.7 percent of its value against the dollar, while the dollar exchange rate, which was 1.30 liras in 2008, leapt to 1.55 liras in 2009.

However, as of 2010, with a fast inflow of foreign investors, the dollar fell again and closed the year 2010 at 1.50 liras. The dollar rose again in the second half of 2011, closing that with an 11 percent loss. The annual average of the dollar was 1.67 liras in 2011.

In 2012, the devaluation of the lira against the dollar remained at around 7 percent, and its average was 1.80 liras.

FED wind It started becoming obvious in May 2013 that the lira was going to devaluate rapidly in 2014. Following the decision by the FED to end their loose money policies, abandon their bond purchases and increase their interest rates, the loss in value of the lira sped up.

Simultaneously, local currencies of several emerging countries such as Russia, Brazil, Mexico, South Africa and India rapidly lost value against the dollar; among them, the Russian ruble experienced an extraordinary devaluation, especially due to the economic sanctions of the United States and its allies and the fall in oil prices.

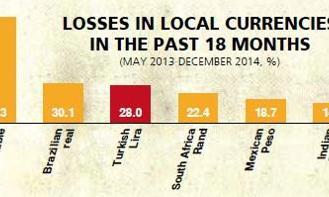

The loss of value in the lira from May 2013 to the end of 2014 reached 28 percent. During this period, while the dollar closed May 2013 with the monthly average of 1.82 dollars, its monthly average in December 2014 became 2.28 liras.

The fall of the lira against the dollar is two points below the 30 percent loss the Brazilian real has experienced. However, it is the Russian ruble that is experiencing the strongest earthquake, actually the disaster, among all the emerging country currencies. The ruble’s loss against the dollar as of May 2013 has exceeded 80 percent. The heaviest blow was experienced in the past two months. In order to slow the erosion of the ruble, Russian monetary authorities are trying all means, including the extraordinary increase of interest rates, but the problem seems to lie in finding a political compromise with the U.S.

The South African rand also, among emerging country currencies, has devaluated more than 22 percent. It is also significant that the Mexican peso lost nearly 19 percent, while the Indian rupee went down nearly 15 percent.

Not likely to descend in 2015 Including the lira, the devaluation of local currencies of emerging countries against the dollar has not come to an end. With the interest rate increasing operations of the U.S. likely to start in the first quarter of 2015, the interest of foreign investors will be lost for countries such as Turkey.

This would mean both a lower growth for an economy that grows with external resources and also a much greater loss in value of the local currencies against the dollar.

In terms of Turkey, the dollar, which will be closing 2014 with an average close to 2.20 liras, is unlikely to start falling in 2015. The lira was troubled when the foreign capital inflow, which was $72 billion in 2013, dropped to approximately $37 billion in 2014. Officials attempted to restrict the dollar’s climb by applying interest rate increases. The dollar/lira parity, which saw 2.40 liras at the beginning of January, prompted the Central Bank to shockingly increase overnight repo interest rates by 5.5 points, up to 10 percent. The climbing of the dollar was stopped with this measure, while its fever went down with the decreasing of the political risk at March 30 local elections. But, again, as 2014 comes to an end, the lira’s annual devaluation is over 15 percent.

In 2015, any increase in the inflow of foreign capital to Turkey is not expected because of the increase in U.S. interest rates and because of economic, political and geopolitical fragilities. Domestic indicators are far from being heartwarming for the foreign investor. Increases in inflation, especially in food products, are showing resistance. Unemployment in September was 10.7 percent when seasonally adjusted; also, it looks as if it will climb further in the coming months. Many experts share the view that the economy, which grew far below expectation in the third quarter, will barely close 2014 with 2.8 percent growth. As a matter of fact, 4 percent was the growth target. This target was revised to 3.3 percent. At the end of the day, growth will be 2.8 percent and this means failure in growth targets.

The unpleasant outlook in economic indicators is also true for political risks. The tension is rising due to 2015 being the year of general elections, the climb in the tension between the ruling Justice and Development Party (AKP) and the Fethullah Gülen community and the fact that the AKP government is in a continuous state of intolerance toward opposition. The ongoing debates on corruption and a lack of laws have even strained relations with the European Union.

All of these are factors that have the potential to discourage foreign investors. When you add the geopolitical risk brought by Iraq and Syria, then there are adequate reasons for foreign interest to drop even further.

As a result, it is expected that the dollar exchange rate, which has had a monthly average of 2.28 lira in December, will continuously climb in the following months of 2015.

Heavy burden on dollar borrowers The nearly 15 percent increase in the dollar exchange rate experienced in 2014 first troubled those institutions that had loans in dollars. Two-thirds of the foreign debts that were announced to be $402 billion in 2014 belong to the private sector and nearly 40 percent of it is due in less than 12 months. This means, for dollar debtors, that in each rise in the dollar, the debts are increasing with no other factor required.

The debtors in the public sector are subject to this burden at a rate of one-third; the real burden will be on debtor banks and private sector firms. It looks inevitable that the 2014 balance sheets of these corporations will contain significant losses from exchange rates. It has been suggested that this may cause serious falls in share prices and that certain banks and companies may demand rescue operations.

As well as making importation more expensive, deterring investments, thus slowing down growth and rising unemployment and causing cost inflation, the hike in the dollar exchange rate will cause other damage at an increasing rate in the coming months, according to expectations.

After 2009

After 2009  Not likely to descend in 2015

Not likely to descend in 2015