Foreign landlords in Turkey need to file taxes by March 25

Diyadin Yakut*

The tax treatment of income elements earned by foreigners from any source of income usually tops the international tax agenda and is extensively debated worldwide by experts, academics and tax experts alike.

In Turkey, too, all tax laws, from the inception of the Turkish Republic to the present day, incorporate the concept of “foreigner” into the technical context of taxation via the definition of tax liability from a taxation standpoint in two distinct ways.

Strictly speaking, tax laws designate tax liability as unlimited tax liability and limited tax liability and proceed to envisage different tax treatment processes for these aforementioned tax liabilities.

Since the subject matter of this article is tax treatment of income derived from the rental of immovable properties and rights in Turkey by limited liable taxpayers (non-residents), it is wiser to confine the scope of the article solely to the definitions made in Turkish Personal Income Tax Law with regard to tax liability and its implications when applied to income gained from immovable properties and rights.

Turkish Personal Income Tax Law (PITL) employs residency criteria to distinguish between unlimited and limited tax liabilities. Residents are, according to the PITL, individuals with legal permanent residence in Turkey and those who reside in Turkey for more than six, uninterrupted months during one calendar year – with the exception of Turkish citizens who live and work abroad for a government agency or a company headquartered in Turkey and still deemed as unlimited liable taxpayers. These individuals are all treated as unlimited liable taxpayers.

Non-residents, on the other hand, are individuals that reside abroad – excluding citizens working for government or a company headquartered in Turkey. Expatriates such as businesspeople, scientists, experts, employees of other governments or journalists who come to Turkey to perform a temporary and definite work, as well as those who have arrived for the purpose of education, medical treatment, rest and travel, are also considered as non-residents regardless of their time of stay in Turkey.

While individuals deemed as unlimited liable taxpayers are subject to taxes on their worldwide income; those who are counted as limited liable taxpayers are only held responsible for their earnings and revenues obtained in Turkey. Accordingly; non-residents, namely limited liable taxpayers, wherever they live and whichever country they have citizenship in, are subject to taxation – within the context of double taxation agreements of course – on their income derived from immovable properties leased in Turkey.

Income derived from immovable propertiesIn Article 70 of the PITL, the income obtained from the renting of immovable properties such as;

Lands, buildings, mineral water sources and underground water sources, mines, stone pits, production places of sand and gravel, brick and tile fields and saltworks;

Large fishing net fields and fishbonds;

Component parts of immovable properties leased separately and all their installations;

Rights registered as immovable property;

Searching, operating and franchise rights and their licenses, patent rights, trademarks, commerce titles, all kinds of technical drawing, design, model and plans;

Copyrights;

And ships and shares of ships and all kinds of motorized shipment-unloading vehicles are deemed as “immovable property income,” and individuals such as owners, tenants, possessors, servitude and usufruct right owners are held liable and responsible for the taxation of that income.

Article 70 states that, income obtained by the landlords from tenants in the form of agricultural products is also deemed as immovable property income.

In the event that the aforementioned properties and rights are rented within the scope of a commercial or agricultural activity, in other words, if these properties and rights are registered with a commercial or agricultural enterprise, the income obtained from the renting of them will be considered as commercial or agricultural income and should be treated according to taxation principles of commercial or agricultural income.

Exemptions and deductionsArticle 21 of the PITL states that immovable property income earners are eligible to benefit from an exemption amount of 3,300 Turkish Liras for the year 2014 provided that they don’t have any obligation to file a tax return due to their commercial, agricultural or professional activities and their total income derived from other types of activities does not exceed 97,000 liras.

Non-resident taxpayers have the opportunity to deduct immovable property-related expenses on two different occasions. They benefit from the right to deduct expenses during the calculation of net amount of income derived from immovable property and later while filing the tax return to determine the amount of payable tax.

The PITL article in question regulates that taxpayers are offered to choose by their free will two different deduction methods to clarify the net amount of income derived from immovable properties: namely lump sum and actual expense methods.

Those who choose to employ the lump sum expenses method have the right to deduct 25 percent of the income as the lump sum expense and are expected not to opt for actual expenses method until two full years elapse.

Deduction of expenses in the actual expenses methodNon-residents who choose to employ the actual expenses method are entitled to deduct expenses such as those pertaining to:

Lighting, heating, water and elevator expenses paid by the lessor for the rented property;

A reasonable amount of management cost relating to the administration of the rented property;

Insurance expenses relating to the rented property and rights;

Interests paid on loans received specifically for the rented property and 5 percent of the total acquisition value of the property for a limited period of five years beginning from the time of acquisition;

Taxes, fees and charges paid to municipalities;

Depreciations;

Repair and maintenance expenses incurred by lessor related to rented property;

Rents and other actual expenses paid by sub-lessors.

Non-residents who choose to employ the actual expenses method for the calculation of net income are expected to keep documents proving expenditures incurred for a period of five years.

Deductions while preparing annual tax returnTo determine the payable amount of tax that will eventually be paid to tax office, taxpayers, at the time of preparing the annual tax return, are granted the privilege of deducting the following expenses as long as they abide by certain restrictions and procedures:

Individual insurance premiums and premiums paid to individual retirement schemes;

Education and health care expenses;

Donations and aids;

Sponsorhip expenses;

Donations in kind and in cash to aid campaigns organized by government;

Donations and aids made in cash to the Turkish Associations of Redand Green Crescent.

Tax withholding, declaration and payment of rental incomeReal persons and legal entities specified in Article 94 of the PITL are held accountable for withholding 20 percent of the rent to be paid to the owners of workplaces they rent for business purposes.

Non-resident taxpayers do not file any tax return with Turkish authorities for their income from immovable properties that is subjected to withholding tax by those specified in Article 94 of PITL, even in the case they have obligation to submit an annual tax return for other types of income elements.

All in all, non-resident taxpayers are expected to file an annual tax return if:

-Their rental income from immovable properties rented for housing purposes exceeds the exempted amount of 3,300 liras for 2014, and

-Their rental income not subjected to withholding tax nor benefiting any exemptions exceeds 1,400 liras, which is the tax threshold to file a tax return for 2014.

If so, the annual tax returns shall be submitted to the tax office that the representative of non-resident taxpayer is registered with or in the case there is no such representation, shall be submitted to the tax office of the province or district that the concerned immovable property is located. The tax return concerning income elements derived during the course of the year 2014 shall be submitted between March 1 and March 25, 2015. The payable tax calculated and eventually assessed shall be paid in two equal installments, one in March and the other in July 2015.

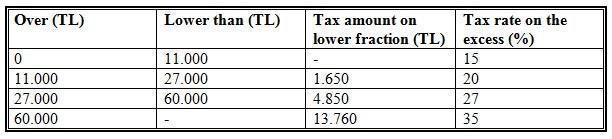

Net income derived from immovable properties and rights demonstrated in the annual tax return after all sorts of deductions and exemptions will be subject to progressive tax rates ranging between 15 and 35 percent specified in the following table for the year 2014.

In terms of double taxation agreementsLike many countries across the globe, inking agreements for the prevention of double taxation of taxpayers that operate internationally with a growing number of jurisdictions (be it bilateral or multilateral), Turkey too, has adopted a standardized framework for all the agreements concluded to date. According to the framework employed, Article 6 of the agreements of prevention of double taxation deals with the tax treatment of income derived from immovable properties and rights by non-resident taxpayers. Article 6 of a typical agreement regulates that income derived by a resident of a contracting state from immovable property situated in the other contracting state may be taxed in that other state, thus enabling the states to have full taxation authority regarding immovable properties within their borders.

Concluding remarksSeveral major factors such as a new law put in place in May 2012 that abolished the reciprocity criterion for the sale of immovable properties to foreigners and lifted some other additional restrictions; recent designation of Istanbul city as an International Financial Center by the Turkish government to turn this city into a regional financial hub; and finally the declaration of grand construction projects within the context of wider urban transformation plans are most likely to attract more and more investors willing to put their money into the Turkish real estate market and make the taxation of income derived from renting of immovable properties by foreigners one of the hottest topics of the tax agenda in coming years.

*Diyadin Yakut is a tax inspector for the Finance Ministry.

The tax treatment of income elements earned by foreigners from any source of income usually tops the international tax agenda and is extensively debated worldwide by experts, academics and tax experts alike.

The tax treatment of income elements earned by foreigners from any source of income usually tops the international tax agenda and is extensively debated worldwide by experts, academics and tax experts alike.