Will a 3-lira dollar lead to an economic crisis in Turkey?

Mustafa Sönmez - mustafasnmz@hotmail.com

Reuters Photo

There has been an acceleration in foreign investors’ exit from the Turkish market after coalition options failed, conflicts escalated in southeastern Anatolia and both the United States and Germany decided to remove their Patriot missiles from Turkey. The Turkish Lira has plunged to around 3 liras to the U.S. dollar. This dramatic loss in the currency’s value was not unexpected, but few expected such a rapid plunge. The unwillingness of the Central Bank to use the rate weapon against this rapid rising trend has made things worse.

Foreign investors have been leaving the country for the last couple of months, pushing the lira into to the ground.

The lira plunged from 2.75 to around 2.9 in the last 10 days. It is likely we’ll see rates over the 3-lira threshold come mid-September, when the U.S. Federal Reserve (Fed) is expected to hike rates. The question is to what extent the economy will endure amid such low levels in the lira’s value. Can the real sector remain robust? Is Turkey falling into an economic crisis?

Ins and outs

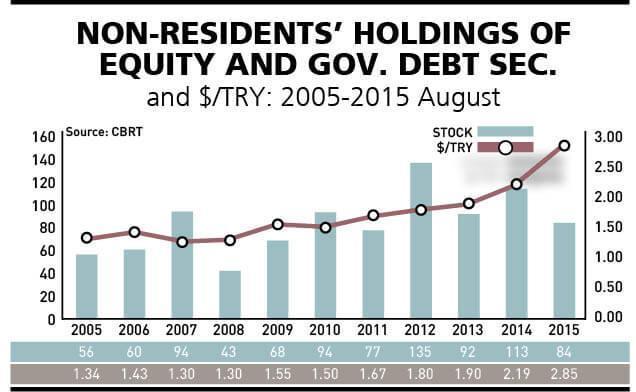

The Central Bank has published how much foreign capital is invested and how much comes, stays or leaves every Thursday since 2005.

These short-term capital moves, which are called portfolio investments, play a great role in shaping the country’s financial balance in general and the exchange rates in particular. The more foreigners convert their own dollars into liras and buy stocks and bonds, the more foreign currency pours into the economy, pushing the value of the lira up. A cheaper dollar enables imports, production levels on imports and economic growth to rise.

The more these foreign investors sell these stocks and bonds and convert to the dollar to leave the country due to instability, the more the dollar’s value increases. This has a negative effect upon consumption, investments and economic growth, and creates serious contractions in the economy. Turkey has been rapidly moving toward this critical threshold in the economy.

Weaker dollar, economic growth

When Turkey was negatively affected by the global economic crisis in 2008 and 2009, there was a huge capital outflow from the country. While foreign investment was $94 billion in 2007, this figure decreased to $43 billion in the following year. With the outflow of foreign capital at $51 billion, the dollar-lira parity surged from 1.3 to 1.5. With the rise in foreign capital inflow in the second half of 2009, parity started to ease again. A total of $94 billion in foreign capital inflow was seen in 2010. This figure rose to record-high levels of $135 billion in 2012. This led to the valuation in the lira and high growth levels. Even the current account deficit increased to alarming levels at $77 billion and economic activities needed to slow down to decrease the gap. The foreign capital surplus was used to support foreign exchange reserves.

Time to exit

Following a gradual rate hike announcement by the Fed in mid-2013, the mode in foreign capital flows has changed for all emerging markets, including Turkey. Things have, however, worsened for Turkey this year. In addition to the rise in economic fragility, political risks and security concerns have been increasing, making Turkey dangerous for foreign capital. This week, foreign capital stocks decreased to $84 billion. On Aug. 8, 2014, a total of $114 billion in foreign capital was in Turkey. We have seen outflow of $30 billion in foreign capital from Turkey over the last year. While the lira was 2.16 against the U.S. dollar, this rate is between 2.9 and 3 today, representing a 34 percent plunge in the lira’s value.

The most foreign capital outflow was seen from Russia and Brazil in 2015 as well as Turkey. Due to this trend, the local currencies of these countries have seen dramatic decreases in value. Some other countries devaluated their own currencies to make them more competitive, such as China, which devaluated the Yuan by around 4 percent. Competitors of China have also made some changes.

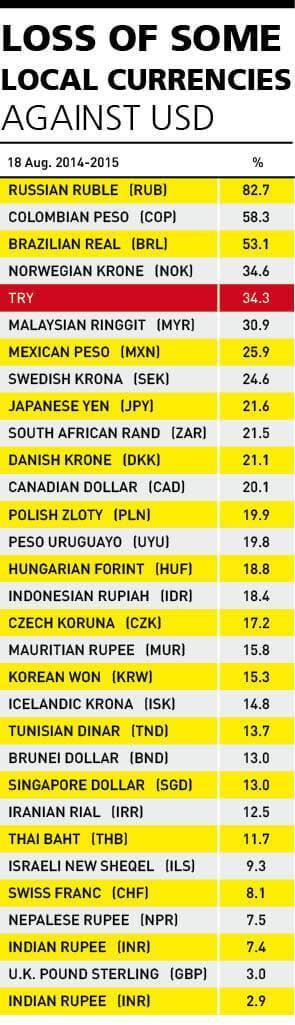

The largest plunge was seen in the Brazilian real’s value against the U.S. dollar between January and Aug. 18 this year with around a 29 percent loss. This was followed by the Colombian peso and the lira by 25.2 and 24.5 percent, respectively.

The smallest loss was seen in the Indian rupee, which suffered a loss of just 3 percent. The currencies of Poland, Hungary and the Czech Republic also lost value of around 4-5 percent. Even the Russian ruble lost value at 5 percent this year after a freefall last year.

The Russian ruble, however, lost 83 percent of its value between Aug. 18, 2014, and Aug. 18 this year. This currency was followed by the Colombian peso and the real at 58 percent and 53 percent, respectively. Norway’s currency lost value of around 35 percent in this period after a devaluation in the country to offset the negative effects of the slump in oil prices. The lira followed it at around 34.3 percent in loss in value...

3 liras to the dollar

The fast outflow in foreign capital has specifically hit sectors which need to pay their debts of $168 billion in the short-term. This amount represents some 42 percent of the total debts. Who is indebted? Some $110 billion of these debts are owed by Turkey’s banks, $54 billion by non-financial companies and $4 billion by the state.

In order to be able to manage this debt burden, they need to refinance their debts at around 3 liras to the U.S. dollar, although parity was around just 2 liras when they took on the debt.

The real sector’s open position is expressed by the Central Bank at around $175 billion. Even with 10 kuruş in losses in the lira’s value, the loss rises by 20 billion liras, making it more difficult to pay debts back.

It is a common assumption that the Fed will most probably hike rates following the Yuan devaluation in September. This will push foreign investors to exit Turkey amid rising political uncertainties and a possible election. The possibility of seeing the lira against the U.S. dollar at beyond 3 liras will rise in this scenario.

Rise in parity and crisis

The rapid rise in the value of the U.S. dollar used to bring real crises in the past. They were, however, no rises in time, but rather devaluations of up to 100 percent in one night. Such steep fluctuations led to serious political crises.

For instance, the 1979-1980 devaluation led to a serious economic crisis followed by the Sept. 12 coup in 1980. They were followed by another steep devaluation in 1994 and economic crisis, which ended the Tansu Çiller government. Turkey saw another plunge in the lira in 1999 and 2001, followed by a serious economic contraction at around 5 percent and the end of Bülent Ecevit’s coalition government. As such, the central right wing collapsed.

It is not wrong to assume that each plunge in currency will lead to an economic crisis and that each crisis will lead to a political collapse. The latest example showing this was the 2009 economic crisis. The global economic crisis serious hit the Turkish economy in 2009, but the government was able to continue sailing thanks to a number of measures.

It is not right to use the term “crisis” to define the turbulence which the Justice and Development Party (AKP) has been experiencing. For instance, Turkey has not yet faced a serious crisis, as opposed to what occurred in 1994 or 2001. The country has, however, been displaying insipid growth numbers. In order to be able to talk about a crisis, there must be negative growth. Turkey has not seen a negative growth trend yet. The country has regressed to 2-3 percent in growth for the last four years, but that is it. We can just talk about the rise of insipid conditions for a country, which used to grow at an average of 5 percent in recent years, but is now growing at just 2-3 percent. This is not a crisis.

General trends

It is obvious that both the rising economic, political and geopolitical risks have made foreign investors uncomfortable. Even if there is not much appealing abroad for investors, the Fed’s possible rate hike in September has attracted all attention. There are also some emerging markets which promise better conditions than Turkey do right now.

It should always be remembered that political actors have the tools to say “no” to the rising negativities, as public finances can especially be used as they were in 2009. The government may not have unlimited powers, but it has the capacity to extinguish possible fires in the economy. Therefore, the government has tightened public finances, limited public spending and eyed new privatization opportunities to find new financial resources.

Nevertheless, the Turkish economy has serious fragilities. The risks to the economy are rising, and at some point, the fire may burn out of control despite all efforts by the Central Bank and resource injections from public finances. This is always a possibility, and this September will especially be very critical.