Turkey under the influence of hot international winds and cold domestic winds

Mustafa Sönmez - mustafasnmz@hotmail.com

AP photo

Interesting days have begun for Turkey and the like “emerging countries.” The central countries have loosened their monetary policies and money is again pouring into emerging countries… This creates the effect of a hot wind…

However, cold winds are blowing in the domestic climates of emerging countries, primarily Turkey. This situation decreases the effect of the hot wind. Nevertheless, those emerging countries with a warmer domestic climate have an opportunity to breathe, even if it is for only a couple of months.

What about Turkey? What do Turkey’s tense political climate, increasing terror barometer and associated non-decreasing risks cause the country to lose? Everybody is curious and debating.

Hot winds

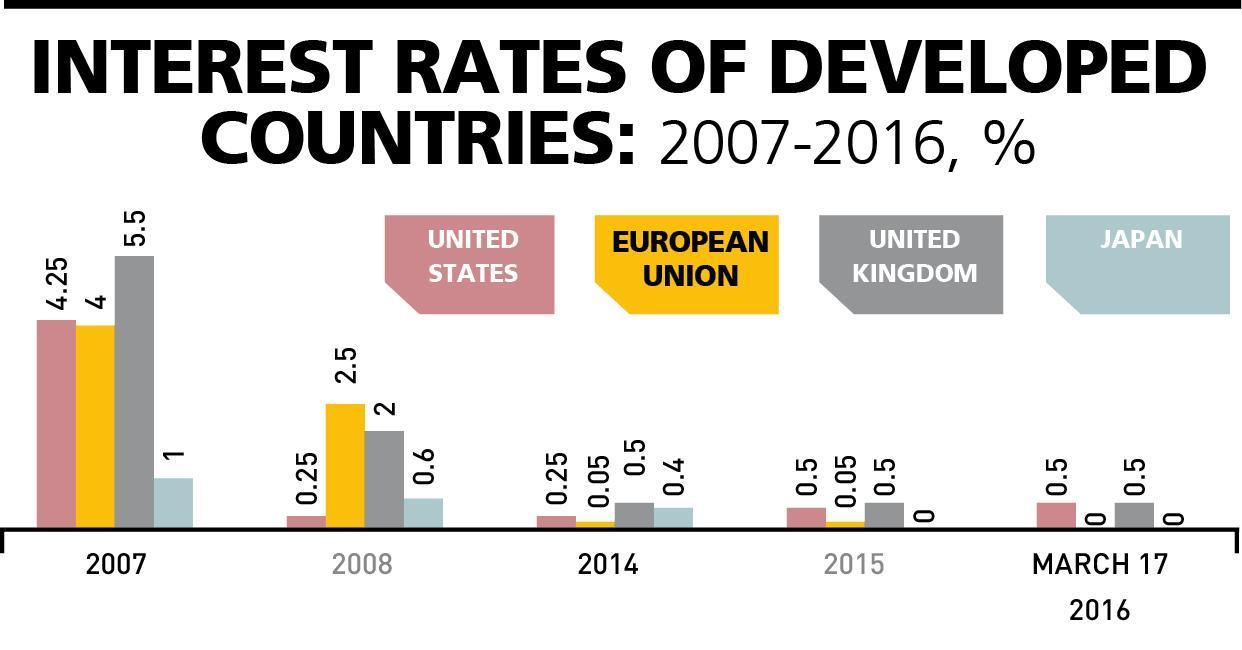

As 2015 was ending, the fear of a repetition of the 2008 shock and the global crisis recurring was widespread. Global markets starting from December 2015 had entered the sales period. Sales intensified in January. In such an environment, even though the U.S. Central Bank (Fed) had made its first rate hike in 2015, it started giving signals that it would hit the brakes. It skipped the hoped for rate hikes in March.

At the end of January the Japanese Central Bank decided on negative interest rates. The European Central Bank announced on Jan. 21 that it would increase monetary expansion. It started this practice in March. Jan. 21 at the same time remained the trough of market deteriorations. Oil prices fell to $27.10.

The policy changes and the verbal guidance of the EU, Japanese and U.S. central banks stopped the downward course. Recovery started in the second half of February.

It became clearer that the U.S., at least for a while, would not hike rates in order to not disrupt the markets. The EU, Japan and China would continue monetary expansion and the negative interest rate practice would go in on. It may be expected that the global risk appetite that was domineering during the month of March together with the warm spring winds of the EU anchor will continue until the start of summer.

The Fed’s gesture

It is as if the Fed, by postponing the rate hike, made the biggest gesture to emerging countries… The possibility of the Fed increasing rates has been a nightmare for developing countries for a long time. It is known that as a result of rate hikes, the capital inflow toward these countries rapidly slows down. Such a development causes a shrinkage of resources, increase of rates and devaluation of local currencies, resulting in a loss of growth momentum.

The negativity caused by the Fed is not limited to only this. All these developments, especially the changes in the foreign exchange rates, cause volatility to increase in these countries. For this reason, almost all emerging countries await Fed meetings with a fearful tenseness. After any meeting when rates do not change, these countries are greatly relieved. When the Fed’s decisions are viewed from this simple framework, then any Fed meeting where rates are not increased is like a gesture to emerging countries.

It is possible to define the method that the global system has discovered and the structure it has formed after the 2008 global crisis against one if its major turbulences as “artificial, temporary and instable.”

However, there is not much of a game plan either. This environment that forms with the steps the Fed takes will continue as long as it operates. There is no prediction about the next move.

Everybody is now focusing on living through this spring without knowing what the summer will bring…

Spring in emerging countries

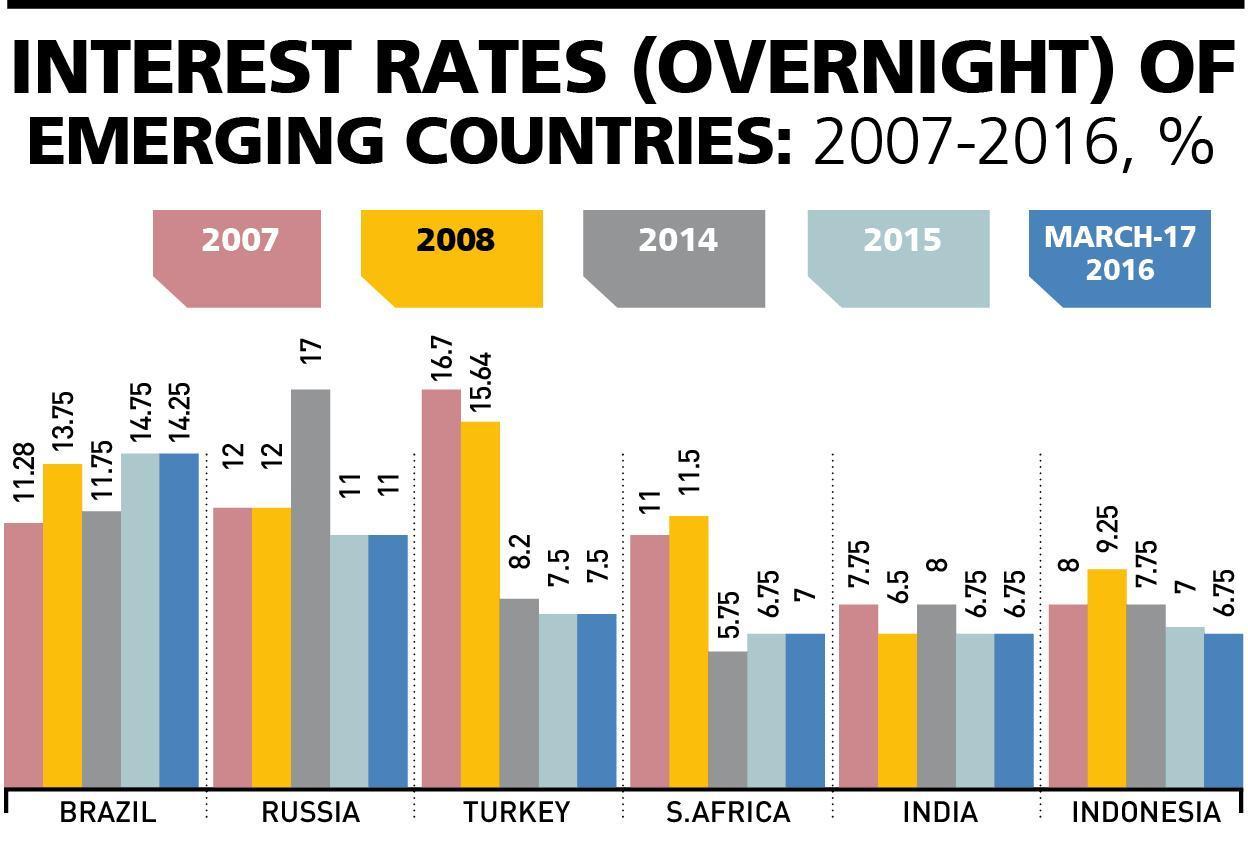

Following the moderate steps in the center, the global risk appetite rose again. Emerging countries are regarded as temporary parking lots. Capital has started flowing to emerging countries, where rates have been kept high since the 2008 crisis. It looks as if emerging countries will continue to be parking lots, at least through the first half of the year.

Because the Fed did not increase rates, the dollar lost value and as a result of this the euro and currencies of emerging countries and gold gained value. The one day loss of the dollar index reached 1.6 percent. The euro on the other hand increased 2.6 percent. The exchange rates of emerging countries according to the JP Morgan Index increased 2.1 percent. Gold prices went up from $1.226 to $1.272 in one day, increasing 3.7 percent.

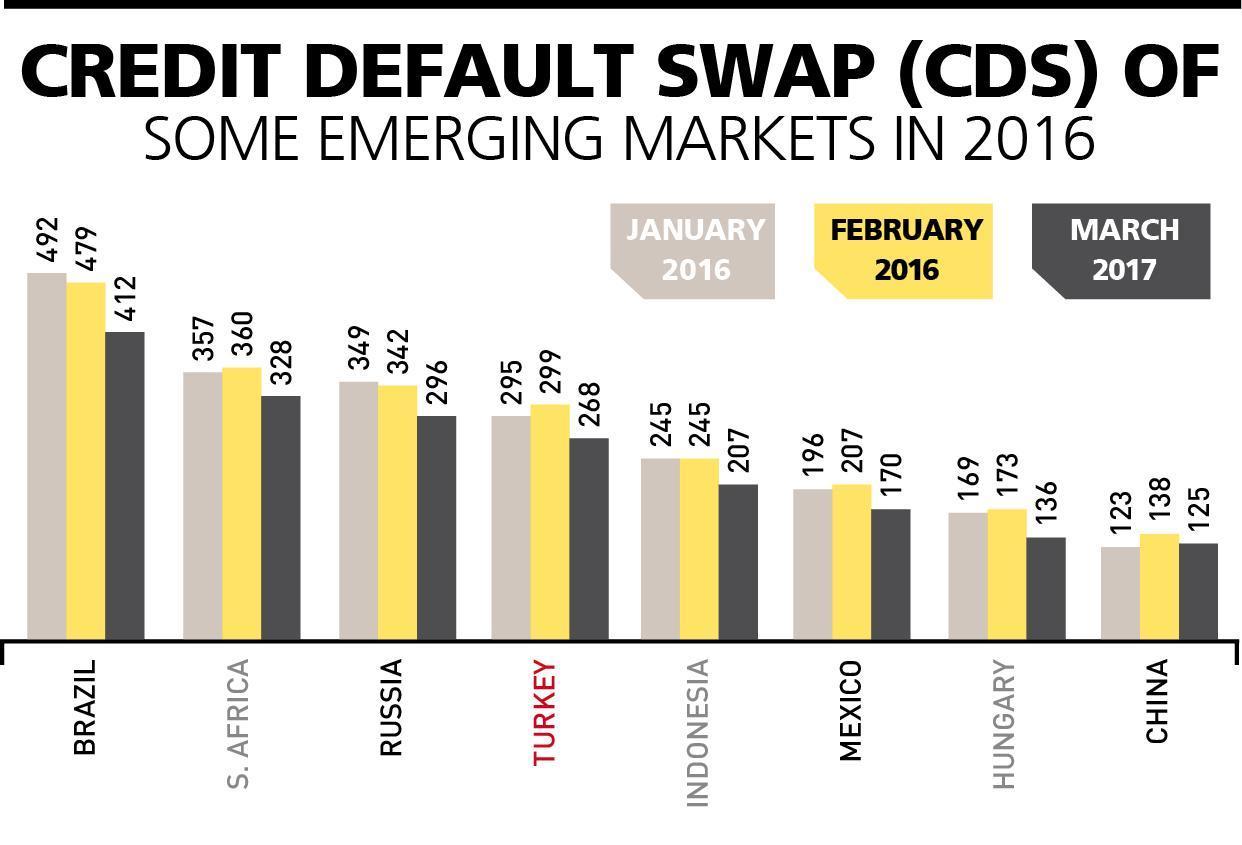

It was observed the risk premiums of emerging countries went down in February and March. The Credit Default Swap (CDS) of Brazil, which has the highest risk, fell 14 percent in mid-March compared to the February average. In risk listing, South Africa is second and Russia is third.

Spring in Turkey

Turkey’s economy also took its share of the international hot winds. The dollar went down to 2.84 against the Turkish Lira around mid-March. Also, 10-year bond rates went down 25 base points to 10.25 percent.

The bourse went above 80,000 points. Turkey’s risk premium, its CDS, was 295 in January and it had an average of 299 in February because of the political and geopolitical tension experienced. It went down to 268 in mid-March. With the effect of these, an early spring began.

From the second half of February until mid-March, when free of exchange rate effects and market price effects, a net portfolio inflow near $2 billion was experienced. With the effect of this inflow, exchange rates relaxed and the price of the dollar, which had peaked on Jan. 22 at 3.05 liras, relaxed in February and March. There were days around mid-March when it went below 2.85 liras.

Cold winds

However, Turkey also has cold domestic winds which immediately chill these blowing, hot winds. They have to be taken into consideration as well. There is the Russian embargo on one hand and on the other domestic terror and the Syrian effect. They are all pressuring the economy from all directions. This effect decreases exports, tourism and contracting services.

The concerns about domestic terror and security have reached dimensions where they restrict domestic tourism, consumption, trade and economic activities. Bombs that went off in Istanbul’s Sultanahmet Square and Ankara’s Kızılay Square, as well as Istanbul’s İstiklal Avenue, have caused the thinning of city centers and crowded venues in big cities, primarily in Istanbul, and has spread fear in citizens who are reluctant to go out on the street. There is a serious stagnation in tourism. It is also observed that people refraining from using mass transportation are jamming traffic.

The effects of all these developments are less consumption, more fear, less production and less generation of services. The potential growth is being restricted. Moreover, payment chains, check payments and loan repayments are disrupted.

Suicide bombs have caused tourism reservations for this year to remain low. Especially congress tourism and Istanbul reservations have suffered huge blows. International meetings and cruise tourism no longer exist.

Business and touristic trips to southeastern and eastern provinces are almost nonexistent and even big cities are affected. The southern resort province of Antalya is affected the most from the Russian effect.

The warm international winds, even though they may be blowing for only a couple of months, should be used as ammunition for future tough times, but this depends on the moderation of the domestic cold winds. The path to this passes through the establishment of a peaceful and democratic climate domestically and regionally. Otherwise, the economy may be vulnerable to the harsh waves that will strike in the second half of the year.