Sleepless nights over Turkey’s foreign currency deficit

Mustafa Sönmez - mustafasnmz@hotmail.com

From the businessperson to the politician, from the debtor to the creditor, everybody’s eyes are on the dollar… These days the dollar is around the level of 3 Turkish Liras and does not seem to be stepping down. It looks like it will settle at around 3.10 liras by the end of October.

International developments - especially the U.S. Federal Reserve’s imminent increase of interest rates - and Turkey’s domestic climate of election speculation, political tension and uncertainty are ramping up risks. When risks increase, the trend toward foreign currency accelerates. Almost 45 percent of money in Turkish deposits has now been converted into foreign currencies. The concern is for this to rise further in a “dollarization panic.” Turkey’s experience shows that this panic state is the most dangerous of all.

International Investment Position (IIP) In the rush toward foreign currency, mostly the U.S. dollar, on one hand there is the tendency of the foreign investor to exit Turkey, while on the other hand there is the non-decreasing demand of companies with foreign currency deficits. How much is the deficit? The answer to that question may be useful in estimating the severity of the dollar’s rise. There are several ways to measure the deficit. One of them is the “International Investment Position” (IIP) to understand a country’s macro foreign currency deficit.

The Turkish Central Bank releases this data every three months. The IIP provides information about a country’s net foreign currency position; it is a scale that shows whether it is in a net deficit or a net surplus, providing information about its ratio to the national income, thus the dimensions of the deficit.

Rapid increase The Central Bank’s data after 2009 show us that Turkey’s foreign currency deficit has been rapidly increasing in recent years. In the second quarter of 2009, there was a $231 billion difference between its foreign currency income and debts and this deficit was about 45 percent of the national income. In the period between 2010 and 2012 when an intense inflow of external capital occurred, the deficit grew rapidly and by mid-2013 it was $424 billion. At the end of that year, its rate to national income was 53 percent: A record-breaking increase.

Starting from mid-2013, with the hike of the dollar exchange rate, the dollar equivalences of liabilities went down. Alongside this, the foreign direct investment inflow also decreased. Thus, Turkey’s foreign currency deficit remained at $431 billion at the end of 2014. This was again nearly 54 percent of that year’s national income.

At the end of the first half of 2015 when the lira’s devaluation against the dollar accelerated and when the foreign investors drew $6 billion, the foreign currency deficit was calculated at $402 billion. This corresponds to a critical level of 55 percent of the national income, which is estimated to have dropped to $730 billion. This shows Turkey’s “dangerous level of fragility,” when the rate is below 50 percent for several “emerging” countries.

Foreign currency deficit of companies We have to look into other data to clarify Turkey’s IIP. This is the data that concerns the assets and liabilities of non-financial companies. What is the foreign currency deficit of companies?

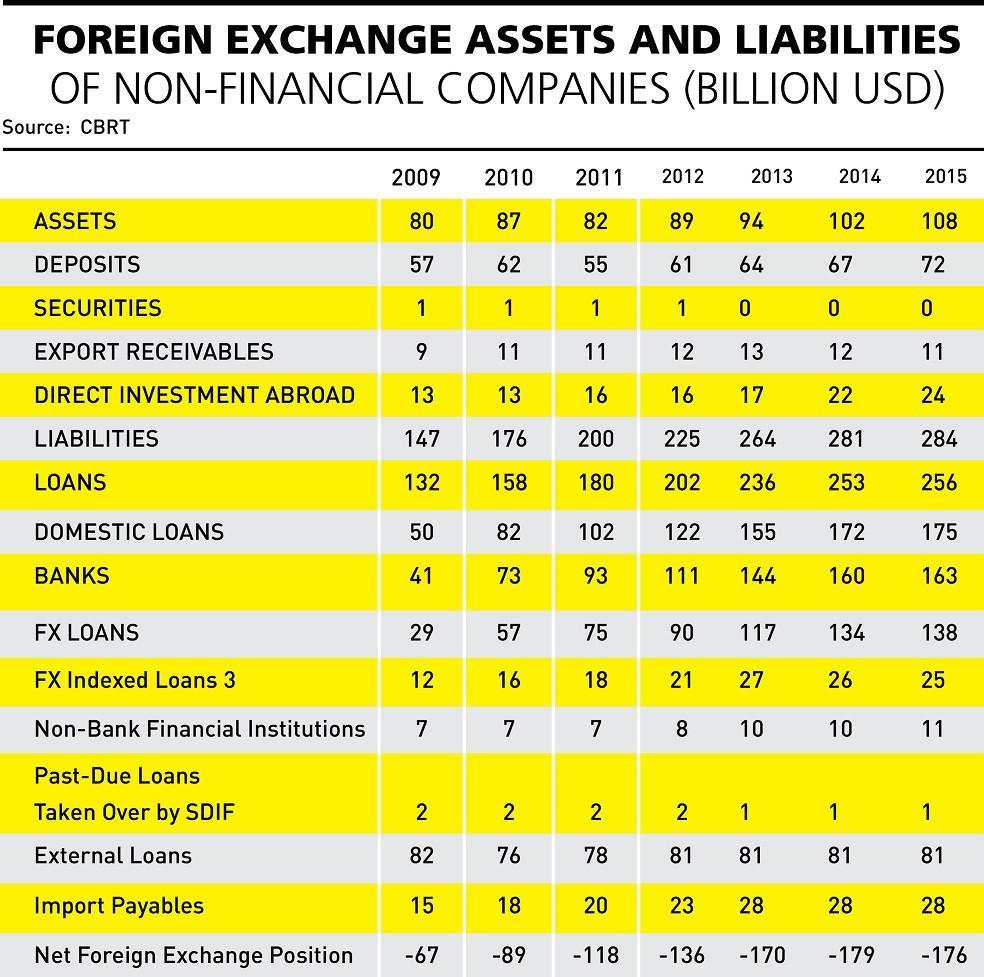

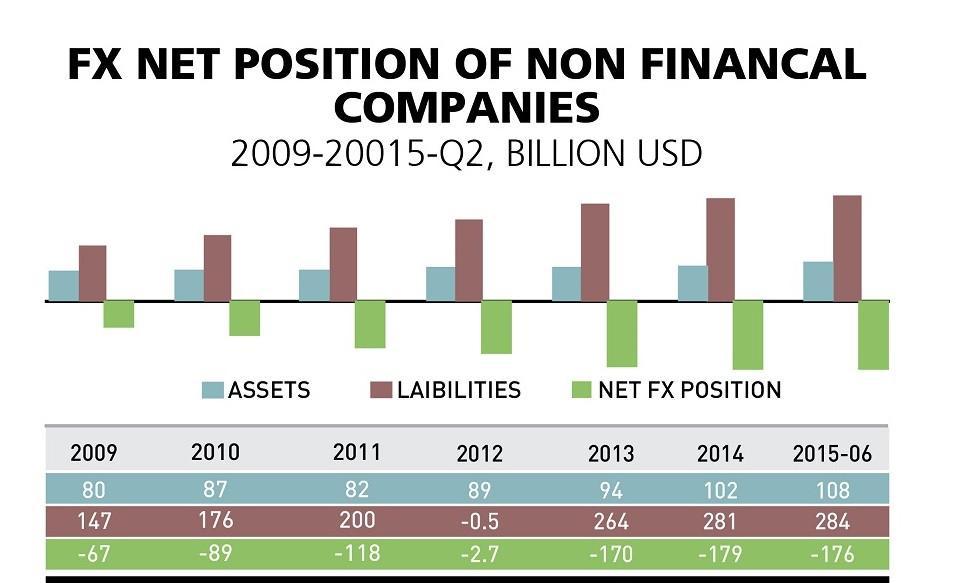

Another statistical data set produced by the Central Bank provides information about the foreign currency risks of companies. Even though it does not have sectoral details, this data set is important because it reveals the dimensions of the foreign currency risks of companies. According to the Central Bank, the deficits of companies after 2009 seem to have rapidly grown. The foreign currency deficit in 2009 was $67 billion, which corresponded to 11 percent of that year’s national income. In following years the deficit and its ratio to national income rapidly increased. The net foreign exchange position of companies was negative $170 billion in 2013 and $179 billion in 2014 - around 22 to 23 percent of national income. The multiplication of this deficit in the past six years is one of the most important factors increasing fragility. The Central Bank reported the foreign currency deficit of companies as being $176 billion at the end of the second quarter of 2015 - around 22 percent of the estimated national income.

According to data, companies have taken $175 billion in foreign currency loans from domestic financial institutions and have $81 billion in debts to international banks. When import debts and other debts are added to the total of $256 billion in debt, companies’ liabilities as of mid-2015 reach $284 billion.

Companies have declared that they have foreign currency assets totaling $108 billion. Two-thirds of this is made up of international deposits. As a result, assets cover only 38 percent of liabilities and companies’ net deficit is therefore $176 billion. This is at a time when the dollar rate is over 3 liras. This is a significant burden on companies and with every climb in the dollar/lira parity they are facing important foreign exchange rate losses.

Which firms? In those companies listed on the Istanbul Stock Exchange (BİST), in their balance sheets their foreign currency assets and liabilities are given in liras. As of June 2015, when the deficits in the lira are divided into an average of 3 lira dollar exchange rate, the 158 companies listed in BİST have nearly $20 billion net foreign currency deficits.

The high negative foreign exchange position of firms may not constitute a definite weakness. For those firms which are open to international trade and which export goods and services, these deficits are manageable. Also, foreign currency assets and foreign currency liabilities of companies should be compared. Those companies with high forex liabilities may also have high forex assets. However, for some companies liabilities have exceeded their assets extensively. For instance, Turkish Airlines looks to have a nearly $4.3 billion foreign currency deficit and its assets cover only 27 percent of them. Turk Telekom’s foreign assets are 8 percent of its liabilities. The same goes for major firms such as Tüpraş, Anadolu Efes, Cola Cola and Torun GYO.

Firms may have objections to this outlook, so the most precise way to address this is for the BİST to inform investors, especially small investors, of this dimension, in order to prevent misinformation or information distortions.

From the businessperson to the politician, from the debtor to the creditor, everybody’s eyes are on the dollar… These days the dollar is around the level of 3 Turkish Liras and does not seem to be stepping down. It looks like it will settle at around 3.10 liras by the end of October.

From the businessperson to the politician, from the debtor to the creditor, everybody’s eyes are on the dollar… These days the dollar is around the level of 3 Turkish Liras and does not seem to be stepping down. It looks like it will settle at around 3.10 liras by the end of October.