Political climate obstructing growth

Mustafa Sönmez - mustafasnmz@hotmail.com

DHA Photo

The European Central Bank’s negative step on interest rates, as well as the U.S. Fed’s postponement of its rate operation, look as if they have created a doping effect on “emerging economies,” which also includes Turkey.

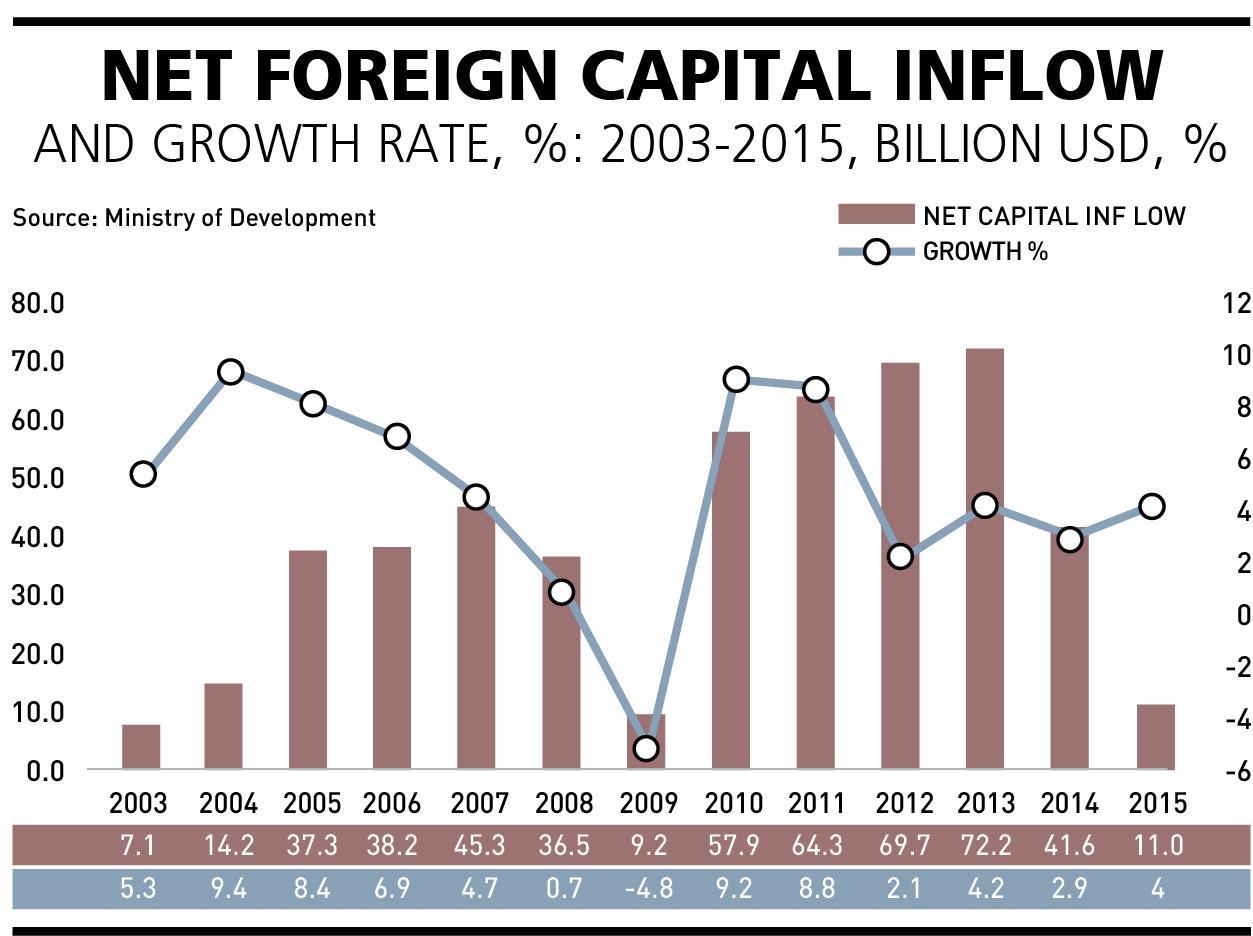

Global funds that withdrew from “emerging economies,” especially in 2015, and took their positions based on the Fed’s rate hikes turned their faces again to their “temporary parking spots” in mid-February.

With this shift, financial prices in emerging economies have moved upward, precipitating a rally. In recent days, the pace of this movement has slightly slowed down but, nevertheless, everybody has started talking about a “spring of the emerging countries,” but its duration cannot be estimated. While the terror that has spread to Europe and the wave of profit realization has disrupted the recent spring atmosphere, this new situation again appears worthy of emphasizing.

Turkey, Brazil, Russia, South Africa, Indonesia, Mexico, Argentina, India… In all these developing countries, recovery signs are continuing. Even though it has not yet been reflected in base quantities, positive expectations for the future have been born…

There is already more talk that developing economies might be able carry this rally to the medium and long term to make a growth leap.

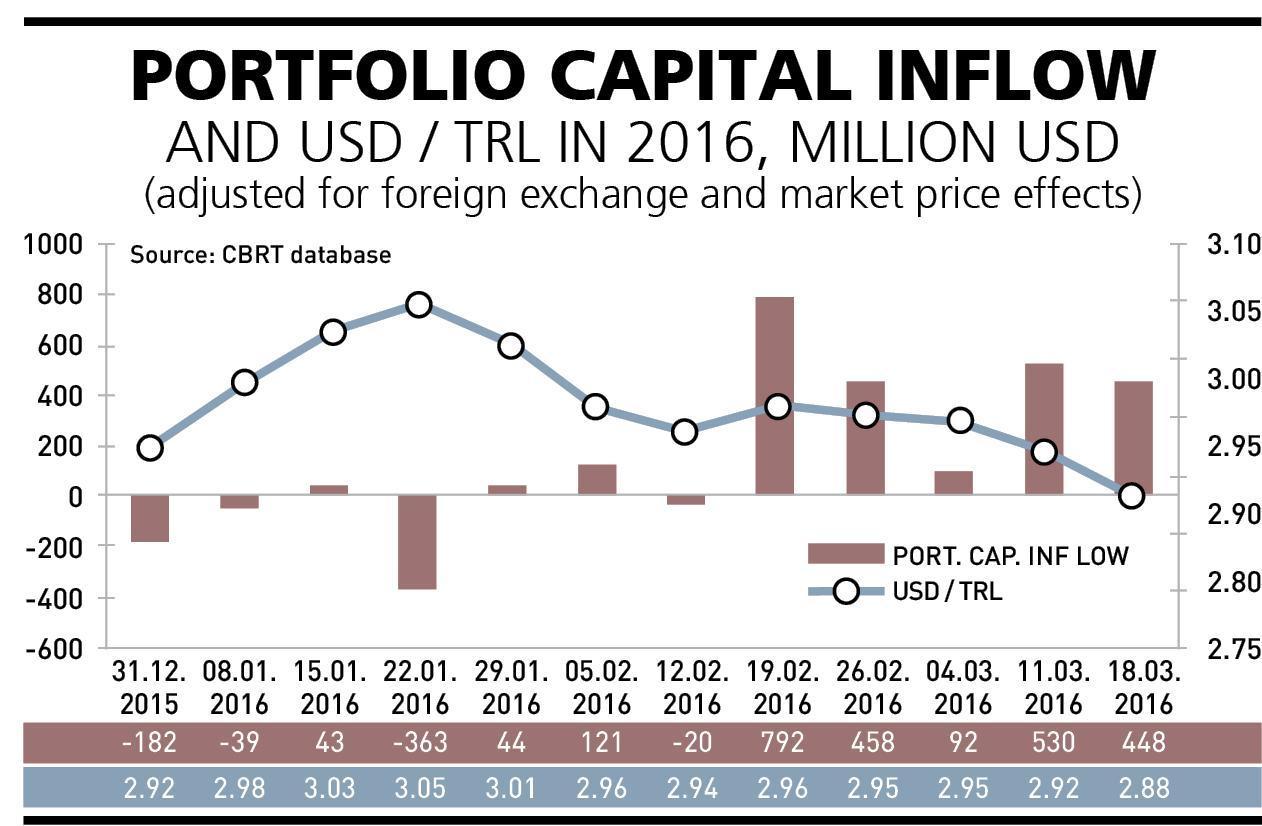

Situation in Turkey In Turkey’s markets as well, movements that go in parallel with this financial rally provoked by global optimism are being experienced. As in developing countries, capital inflow has accelerated. Until mid-February, instead of foreign net inflows, withdrawals were observed – something that was dominant in 2015. When calculated free of the foreign exchange and market price effects, from mid-February until mid-March, a net capital inflow of $2.5 billion was observed.

With this inflow, as expected, the Turkish Lira gained value. The dollar peaked at 3.05 liras on Jan. 22, and then started going down. With net capital inflows, 1 dollar went down to 2.88 lira in mid-March.

With this development, market interests fell. The Central Bank’s average funding interest rate also joined and fell 25 base points. Asset prices went up. In parallel with these, expectations rose that foreign capital investment in Turkey would increase.

The same question for other emerging countries is valid for Turkey as well: Is it possible for Turkey’s economy to carry this rally further and convert it into a real recovery?

Some think that this transformation could easily be done. Moreover, some even say that Turkey’s economy might be able to positively differentiate itself from other developing countries.

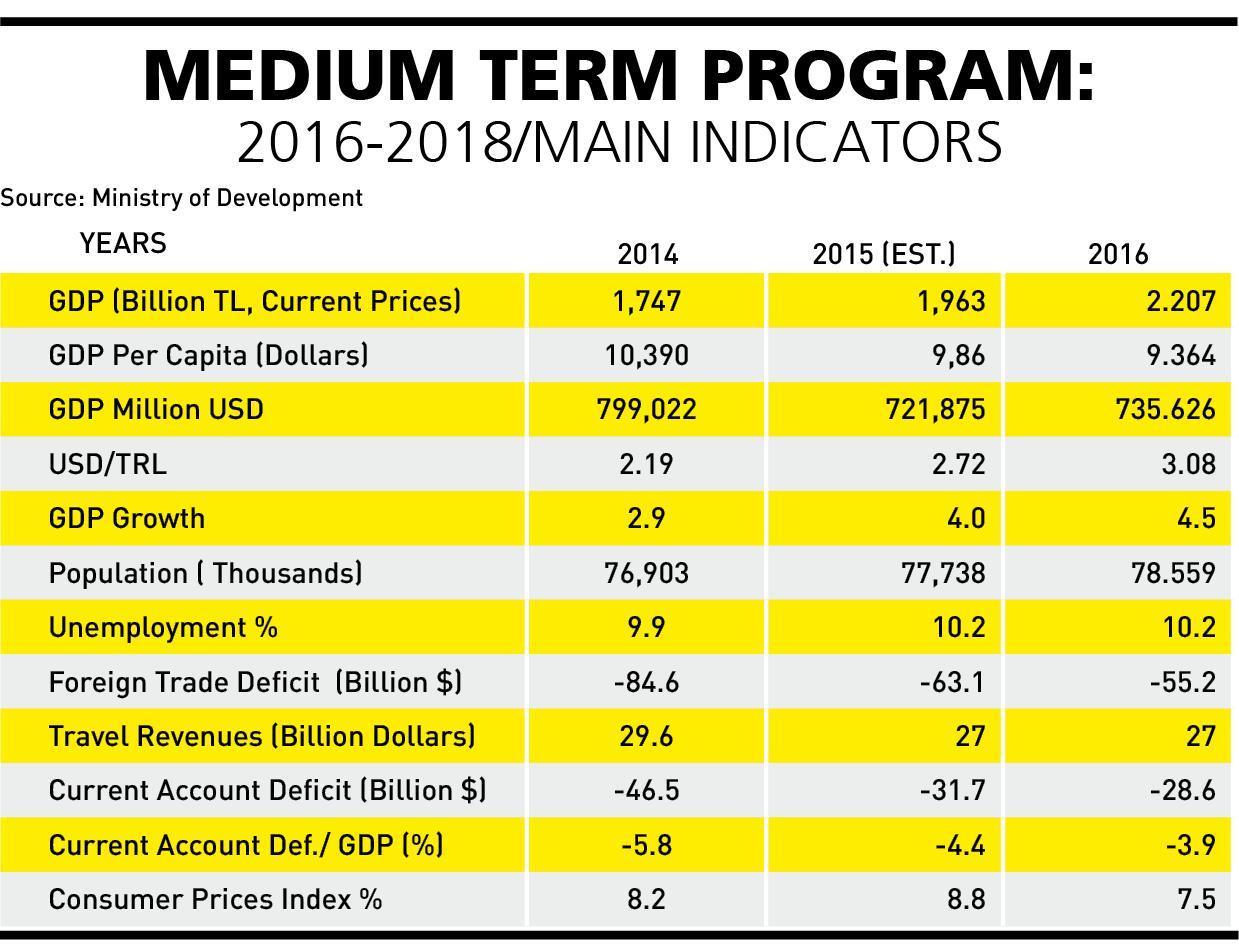

Medium targetsWill the negative interest rate in the European Union and Japan and the situation created by the cautious interest rate in the United States help Turkey meet its 2016 targets?

According to the Medium Term Program (OVP), the growth rate target is 4.5 percent, inflation 7.5 percent and unemployment 10.2 percent. One obstacle is falling tourism revenues. Russian sanctions and the worsening image of the country are others.

A calm assessment could be that the structural weaknesses in Turkey’s economy are continuing. Together with the added economic and geopolitical negativities of the period, it is unlikely that this rally will turn into a growth trend.

The lack of savings is at the top of the list of Turkey’s economic vulnerabilities. This shortcoming will cause the investment performance of Turkey to become dependent on foreign resources.

Low demand When we look at the demand categories that would support growth, the situation is not pleasing either. Both domestic and foreign demand have not fully recovered. Foreign demand is affected by international developments as well as domestic developments. Exports and imports have slowed down at the same time. The slowdown in imports is because of the halt in the growth rate and the halt in investments. The drop in oil prices lately has dropped the energy bill which contributes to the overall nominal decrease. Exports, on the other hand, are to a great extent associated with Turkey’s market losses in neighboring countries, with the losses in the Russian and Iraqi markets particularly striking.

While commodity exports have slowed down recently because of the impasse especially in tourism, there is a loss in service exports.

All of these are not issues that can be corrected by the financial rally. Thus, there is not much hope from foreign demand. Domestically in terms of public finances, even though the Medium Term Program has ventured some spending, the budget deficit in the program is not projected to exceed 1.5 percent. The most important component of the situation facing the international audience is the central budget – fiscal discipline. The administration does not want to weaken this.

In the monetary zone, interest rates are relatively high. The highness of the inflation is preventing the loosening of money and a decrease in the interest rate. On the other hand, the high-level course of both economic risks and geopolitical risks is forcing the interest rate upward. These are all trends that are not likely to change with the fact that the interest rate climate seems to be recovering.

Expectations The vulnerability of Turkey’s economy is increasing with the disruptions of recent expectations. The latest trends in expectation surveys show that the disruption has increased. There could be many reasons for that, but the most important is the tensions nurtured by politics and the climate of clashes.

The clashes in the southeast since June 7, 2015, that resemble a covert war, together with the massacres and terror acts in big cities that have sent everyone inward have all increased Turkey’s political risks. The tension ongoing in the geopolitical arena is also important.

Now, the arrest of businessman Reza Zarrab in the U.S. for money laundering has been added to this. The legal process that started with this arrest is likely to have reflections in Turkey. There are loud suggestions that this operation could force open closed files in Turkey. The pro-government media has interpreted this as a coup attempt by the U.S. against the government.

In these circumstances, it is difficult to motivate local or international business leaders to undertake new investments and new decisions. It is also not easy to convince all kinds of consumers to consume and use loans for consumption.

In such an environment, it does not seem very easy to turn the financial rallies that have been formed with the winds blowing from outside into chances for growth.