Not much ROCing around the clock

When the Central Bank first started using its Reserve Option Mechanism (ROM), it was touted as the ultimate answer to exchange rate volatility.

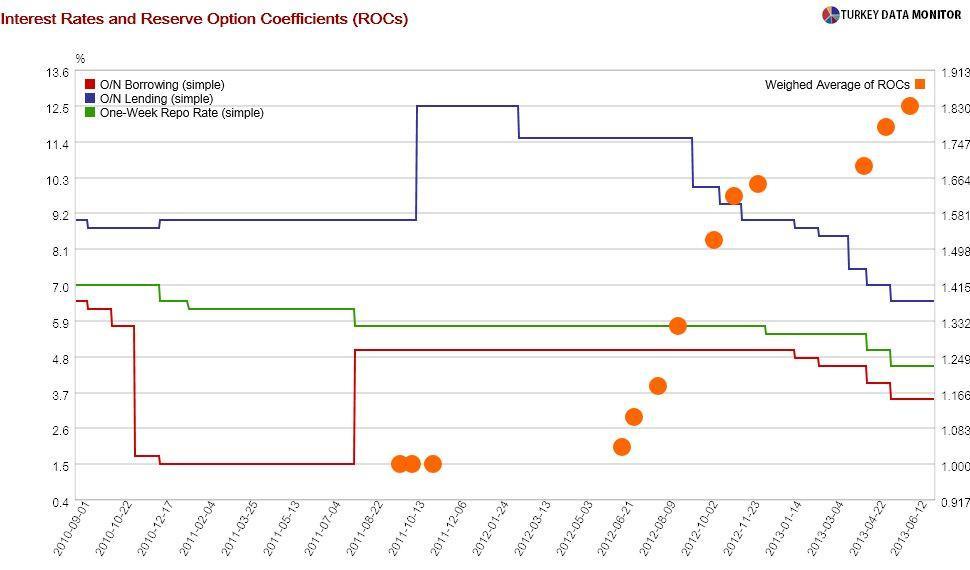

Banks have been allowed to keep some of the lira reserves they are required to keep at the Central Bank in foreign currency (FX) and gold since 2011. In May 2012, the Central Bank increased the upper limit of this option to 45 from 40 percent of total required reserves. It also noted that this last 5 percent would be multiplied by a coefficient of 1.4, so 100 liras of reserves could be replaced with 140 liras worth of FX. Since then, the Bank has been “experimenting” by increasing the upper limit gradually and introducing different Reserve Option Coefficients (ROCs) at different tranches.

It was expected that ROM would work as an automatic stabilizer. It would take some pressure off the lira during strong capital inflows. And when this hot money stopped or reversed, banks could tap their FX reserves at the Central Bank, providing a line of defense against depreciation.

When I discussed the mechanism in September 2012, I argued that it should be seen as a supplementary tool at best.

Just as I felt it could not take the heat off the lira by itself, I was not sure it could withstand an episode of major capital outflows.

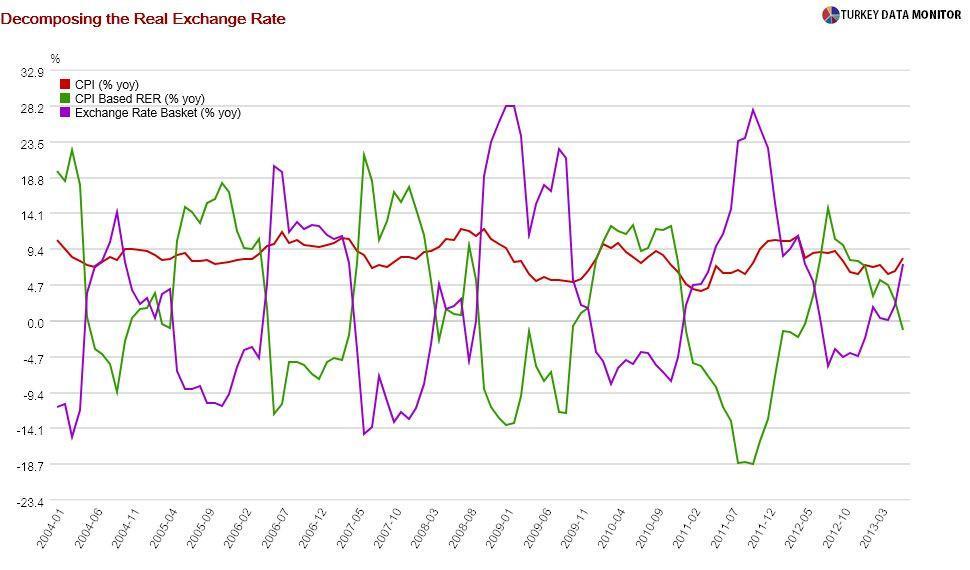

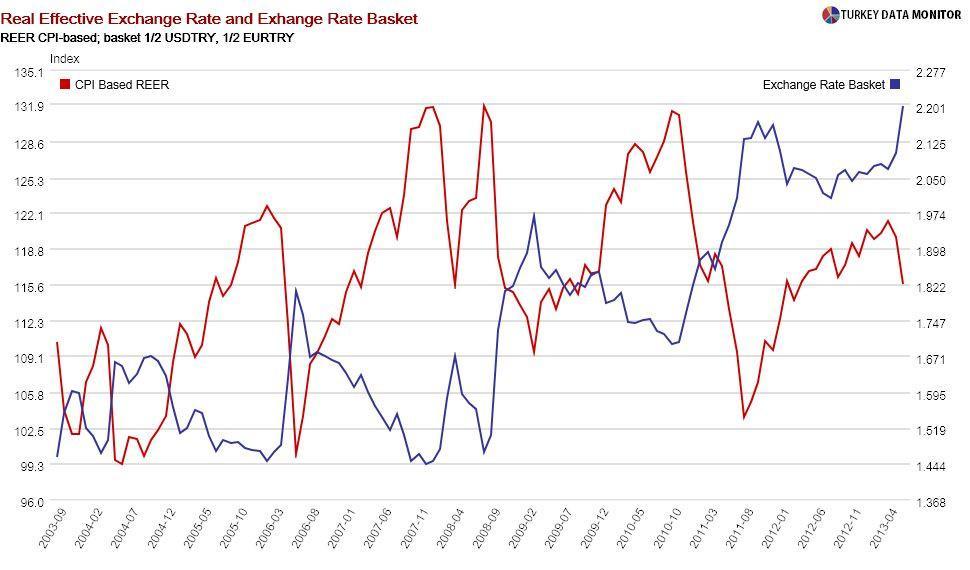

Since most of the real lira appreciation was from Turkey’s inflation differential with developed countries, I always felt that the best way to prevent an overvalued currency was by keeping inflation low rather than tampering with the nominal exchange rate. Leaving this aside, the Central Bank was indeed able to prevent excessive lira appreciation, although it is impossible to discern ROM’s contribution.

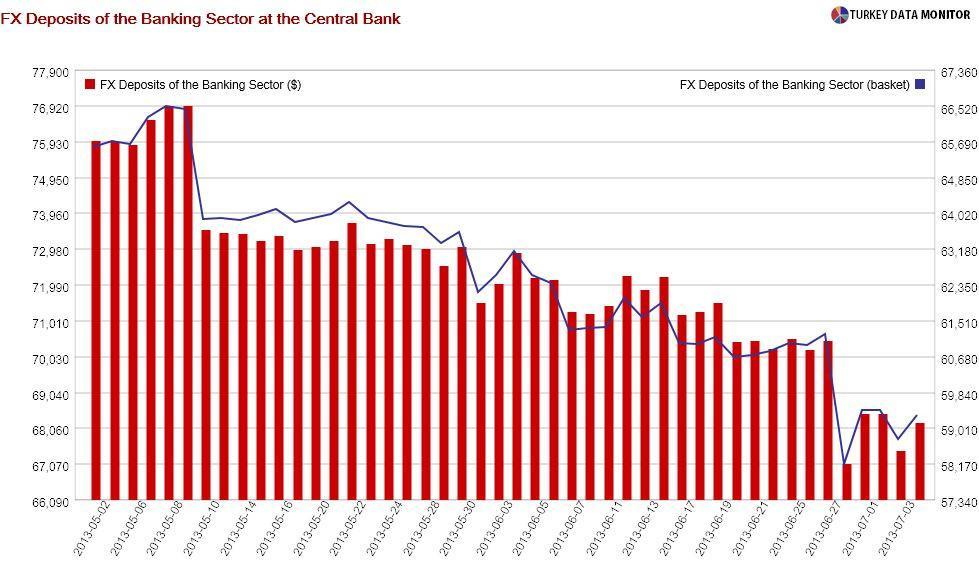

But the Bank’s ingenious mechanism was never tested against capital outflows- until last month. Looking at commercial banks’ FX deposits at the Central Bank on a weekly basis could give us an idea on ROM’s performance. These deposits decreased from $ 73.2 to 71.5 billion at the end of May. After hovering in the $ 71.5-72 billion range for a couple weeks, they fell by another $ 5 billion, $ 2 billion from June 14 to 21 and a further $ 3 billion the following week.

Banks decreased their ROM reserves at the onset of the turbulence and then in the second half of June, not during the height of the turmoil. Besides, the decrease from June 21 to 28 is entirely due to revaluation from declining gold prices. Although we don’t have last Friday’s data yet, we could say that ROM helped, but not as much as the Central Bank had hoped.

This is not surprising. For one thing, banks can access their FX reserves at the Central Bank only every other Friday. That’s why the Central Bank has sold $2.65 billion of FX since June 11. Moreover, to utilize ROM reserves, banks would need to open short FX positions, which they have traditionally been reluctant to.

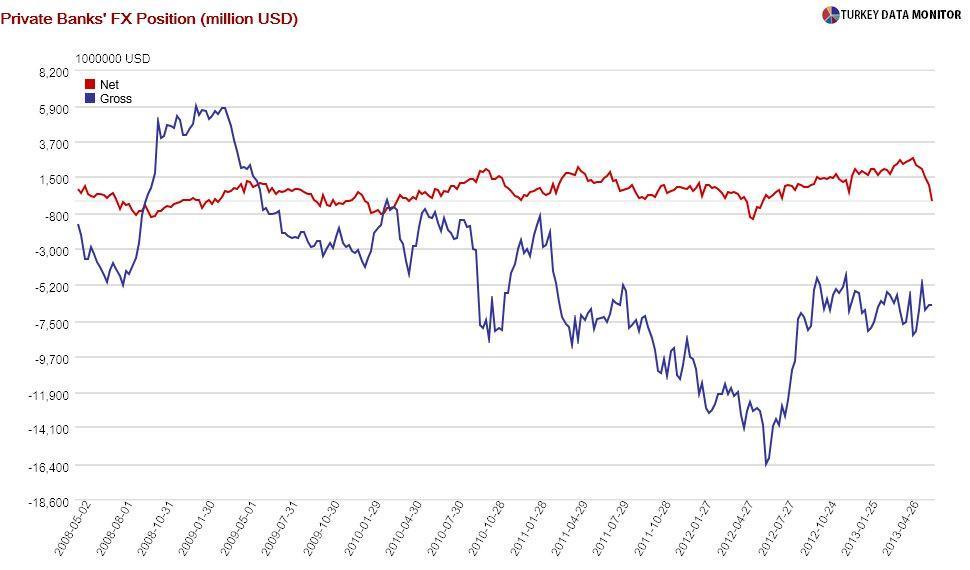

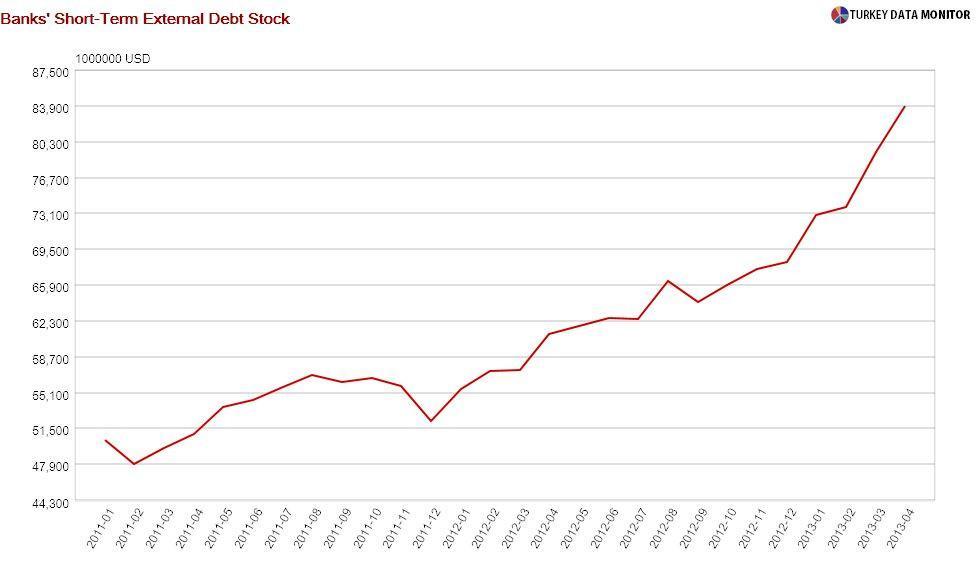

There was one thing ROM was very successful in. Banks’ short-term external debt has skyrocketed, but I am not sure the Central Bank was intending that.

When the Central Bank first started using its Reserve Option Mechanism (ROM), it was touted as the ultimate answer to exchange rate volatility.

When the Central Bank first started using its Reserve Option Mechanism (ROM), it was touted as the ultimate answer to exchange rate volatility.