Turkey’s banks at ease while industry stresses

Mustafa Sönmez - mustafasnmz@hotmail.com

Turkey’s economy is going through a tough period with the buildup of risks in the economic, political and geopolitical climate. Nevertheless, concerns about the future of the economy vary from sector to sector. As a matter of fact, it also varies depending on the size of the enterprise. For instance, big holding companies that are operating in various sectors have relatively minimized their risk by putting their eggs in different baskets. Even if they lose in industry, they win in finance or real estate…

The banking sector is especially less affected by the ongoing tension and has been able to maintain its profitability at a certain level.

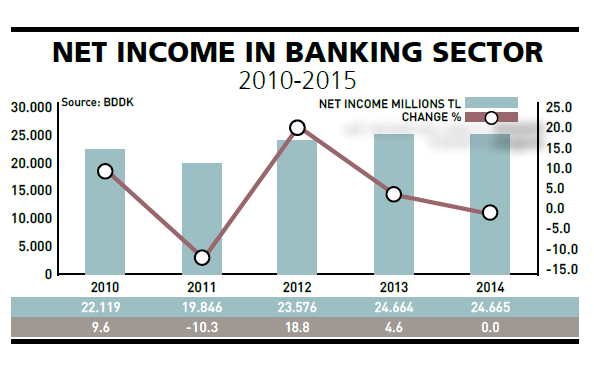

The situation for the 50 banks that make up the backbone of finance is for instance not as sorrowful and gloomy as industry. On the contrary, the banking system rapidly recovered from the interest rate turbulence of 2014 and has been able to increase its net interest rate income from 52 billion Turkish Liras in 2013 to 57 billion liras in 2014, maintaining its period income at 24.7 billion liras.

From the bank profits data of the first half of this year, we understand that the banks are doing well.

According to data from the Banking Regulation and Supervision Agency (BDDK), the first half profit of the banking sector increased 11 percent compared to the same period last year and reached 13.8 billion liras. This is regarded as a sign that this entire year will end with a net profit of over 26 billion liras.

The banking system, with its 12,213 domestic branches and 87 branches operating abroad, is hiring more than 218,000 personnel, including the overseas ones. The system has around 45,000 ATMs and it is known that private and foreign banks in particular have a high rate of profit.

Statements made by bank managements in the first half also pointed out that they were quite content. For instance, in the first six months of the year, İş Bank General Manager Adnan Bali - the net period profit of the first six months of the year was 1.82 billion liras - said, “İş Bank, also in the second quarter of the year has successfully applied its growth policy and has raised it size of assets to 268.3 billion liras, continuing to be the biggest private bank of Turkey.”

Other banks, including Akbank, Garanti Bank and Finansbank, are all also happy… But, only for now…

Under control

Turkey, in the economic crises it went through in 1994 and in 2011, received big blows in the banking sector. In the 1994 crisis five banks and in the 2011 crisis 20 banks were handed over to the Treasury with public intervention, undertaking heavy public damages. With lessons drawn from these experiences, the banking system is now much more under control.

In the sector, the activities of 50 banks, 33 of them deposit banks, 13 of them development and investment banks and four of them participation banks, are under daily scrutiny.

The size of assets of the sector was 2 trillion liras as of the end of 2014, which increased 8.4 percent in the U.S. dollar base, corresponding to $862 billion.

The share of public banks in the sector’s total assets was 31.4 percent, while local private banks had a share of 49.5 percent and foreign capital banks had a 19.1-percent share. In terms of assets, deposit banks had 90.4-percent share, participation banks 5.3 percent and development and investment banks 4.3 percent.

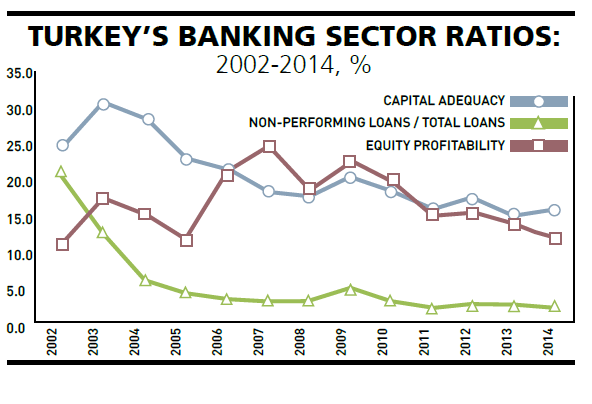

Regarded as the boss of the banking system, according to the BDDK, with the stress tests done, with its strong capital structure and other indicators related to its risks, the sector continues to prove resilient to macroeconomic shocks.

Industrialists

Messages saying “Everything is under control” for the banking system have been received, but can the same thing be said for industry? Istanbul Chamber of Industry (İSO) head Erdal Bahçıvan said the situation was not so bright for those firms who have anchored in industry. He also said, “One of the most significant parameters on whether the financial structure of companies is healthy is the ratio of total debts to equity capitals. This ratio was high, as it was last year at 132 percent.” He also drew attention to the emphasis on low-technology in industry.

According to 2014 data, low-technology usage was 40 percent, medium-low technology usage was 37 percent, medium-high technology usage was 19 percent and high technology usage was 3 percent. Not even 1 percent of sales were allocated for research and development (only 0.7 percent). The number of joint foreign capital institutions fell to 126 in 2014.

The operating profits of the top 500 major industry companies decreased 6.4 percent to 30 billion liras compared to the previous year. Bahçıvan said, “The main factor for us is the operating profit of the industrialist. It is quite thought-provoking that this figure has gone back. Non-operating means had a positive effect on the increase of profits of industrialists. However, the profitability from the main activity of industry should never be pushed into the background.”

Many industrialists, with a correct estimation that the dollar would gain value against the lira, have compensated a portion of their losses by investing in the dollar. This is the non-operating profit Bahçıvan referred to.

While profits directly from business reached 36 billion liras in 2013, this figure went down to 30 billion liras in 2014. If you also take into consideration inflation, it is a fall from real profits.

External commitments

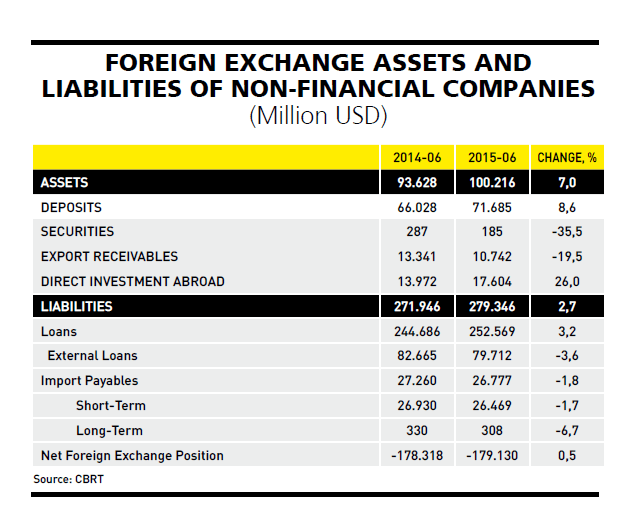

The net exchange position which shows the difference between foreign exchange as assets and liabilities of non-financial companies, in other words the real sector, has a structure which leaves many sleepless.

Real sector companies had $94 billion in assets 12 months ago and this figure went up to only $100.2 billion in May 2015, but in the same period their liabilities reached $279.4 billion.

In other words, the asset-liability difference is $179.1 billion. Even if the real sector wanted to use all its assets to pay off all its liabilities, it will again have a debt of $179 billion.

At the end of May, the dollar exchange rate was around 2.66 liras. The average of August is around 2.76 liras. In other words, the 10 kuruş increase in the dollar has increased the net foreign exchange position of the real sector at least 18-19 billion liras. This much of an exchange rate loss has been recorded in balance sheets…

At this rate, it is possible to have the dollar/lira rate to settle at the 2.80 band, as a matter of fact, according to some others at the 3 lira band. The problem is not at the band but that this band was reached in a very short time.

With the policies adopted for years, the government directed the private sector to loan in foreign currency and to use foreign loans, and then this time very different domestic and external developments caused the exchange rates to hike rapidly.

Inevitably, there will be stumbles in the real sector, industry and construction. There are stumbles already but no high-profile knockouts. But it is known that a serious knockout would turn into a chain accident and the banking system would be damaged.

Political measures, primarily political stability, is a must to curb the uncontrollable hike in exchange rates, and then the economic and geopolitical risks have to be decreased so that at least a part of the outgoing foreign investors would come back, decreasing the risks, enabling the dollar rate to remain in a less problematic band…

Turkey’s economy is going through a tough period with the buildup of risks in the economic, political and geopolitical climate. Nevertheless, concerns about the future of the economy vary from sector to sector. As a matter of fact, it also varies depending on the size of the enterprise. For instance, big holding companies that are operating in various sectors have relatively minimized their risk by putting their eggs in different baskets. Even if they lose in industry, they win in finance or real estate…

Turkey’s economy is going through a tough period with the buildup of risks in the economic, political and geopolitical climate. Nevertheless, concerns about the future of the economy vary from sector to sector. As a matter of fact, it also varies depending on the size of the enterprise. For instance, big holding companies that are operating in various sectors have relatively minimized their risk by putting their eggs in different baskets. Even if they lose in industry, they win in finance or real estate…