Very moody after Moody’s upgrade

You probably already know that credit rating agency Moody’s

upgraded Turkey to investment grade (IG) late on May 16.

Markets were expecting it, as it would eventually come after Fitch upgraded Turkey to IG in November. Turkey’s peers got their second IGs in 11 months, on average, after the first one. Although driven by loose domestic and international monetary policy as well, the recent strong capital flows are typical before a second IG, according to

a Central Bank of Turkey research note.

Moody’s noted that the key drivers of the rating action were: “1) Recent and expected future improvements in key economic and public finance metrics. 2) Progress on structural and institutional reforms that Moody’s expects will reduce existing vulnerabilities to shocks to international capital flows over time.”

We have

yet to see the reforms Moody’s is referring to. And although this is the first time I’ve seen an upgrade based on what is yet to come, the rating agency is right that Turkey has made

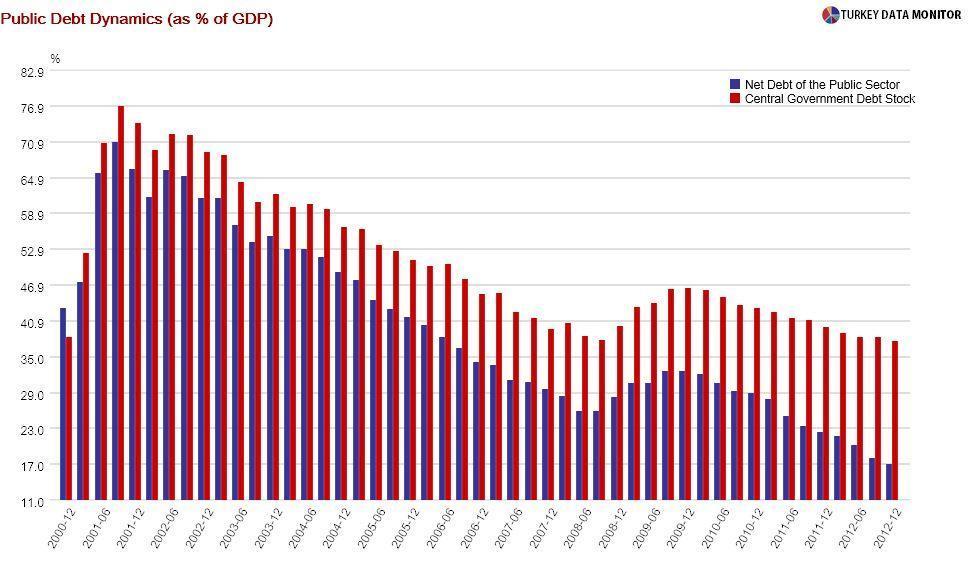

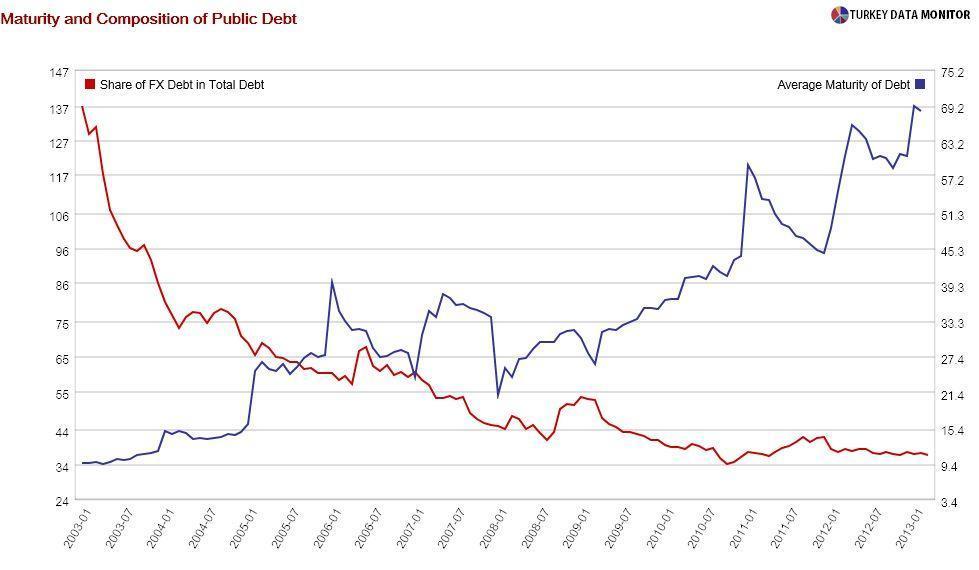

key improvements in public debt management, not just since 2009 as they are noting, but in the last decade. As they emphasize as well, not only the debt burden has fallen, its maturity has risen and the share of debt denominated in foreign currency has declined.

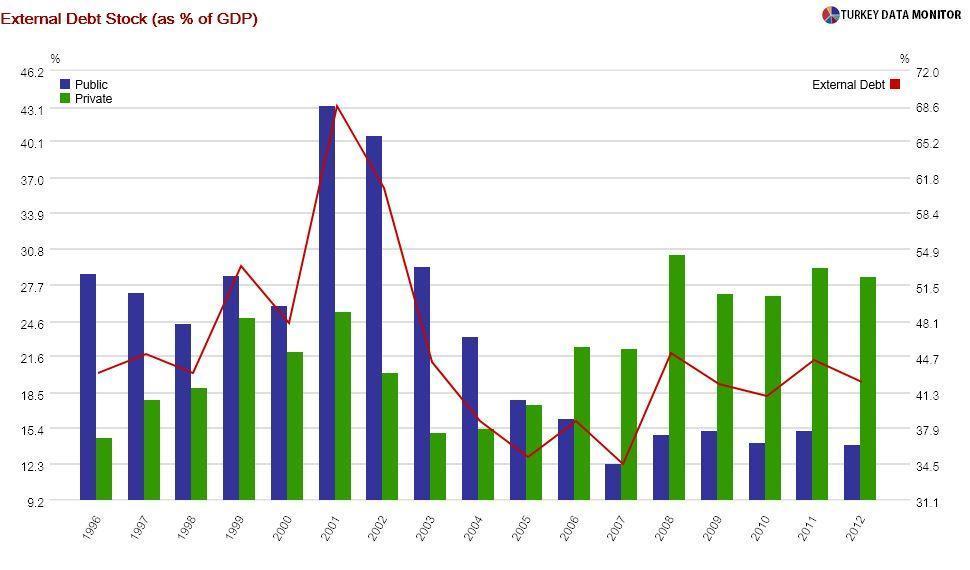

Turkey reached an important milestone when it

paid off its debt to the IMF on May 14. Unfortunately, public external debt has been

replaced by private external debt. With the exchange rate virtually fixed by the Central Bank, it makes sense for

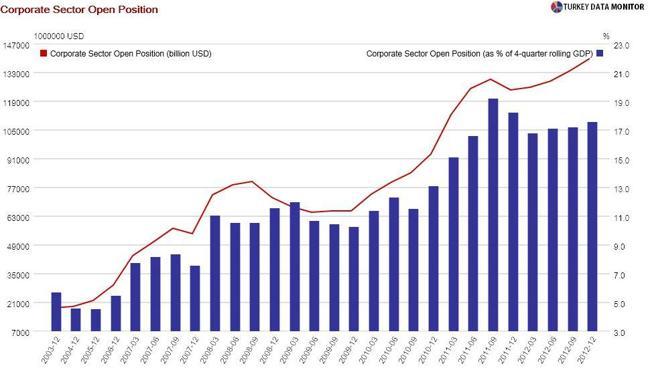

corporates to borrow in foreign currency, and their open positions are nearly $140 billion as of the end of 2012.

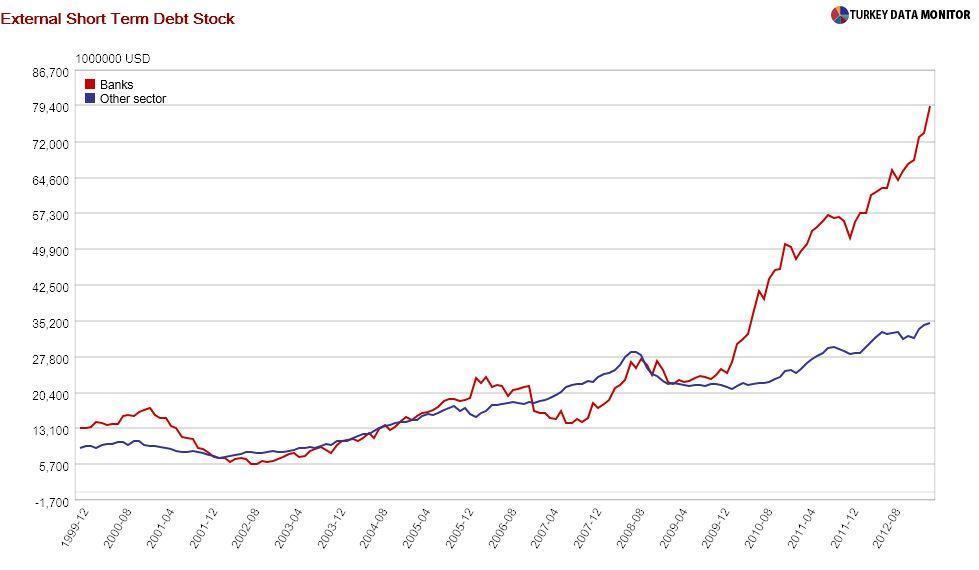

In fact, banks’ short term external debt has surged since the 2009 Moody’s benchmark. It has recently been on the rise thanks to the Central Bank’s

reserve option coefficients, as banks are induced to borrow in foreign currency for use as part of their required reserves. The latest data released on May 17 revealed that it rose by almost $6 billion in March alone.

In fact, Moody’s is well aware of these risks. It noted that the country’s “external vulnerabilities are generally greater” than most of its peers. So are investors: A hedge fund manager recently told me that Turkey usually comes up as one of the top three risky countries in investor meetings. The upgrade is likely to make this situation worse by increasing dependence on external financing.

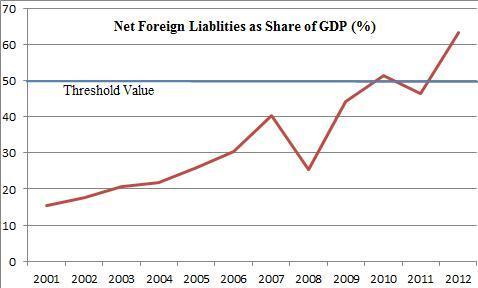

An IMF paper released a few hours before the upgrade finds that “the ratio of net foreign liabilities to GDP is a significant crisis predictor, and the more so when it exceeds 50 percent in absolute terms.” Economist Tolga Dağlaroğlu calculated that ratio for Turkey and found that it jumped from 46 to 63 percent in 2012.

The Central Bank has the tools to respond, but at their latest meeting with economists on May 17, they did not seem worried about an unexpected sudden stop, or an eventual halt when advanced country central banks begin to tighten liquidity, to capital flows. That’s why I am so moody after the Moody’s upgrade.

You probably already know that credit rating agency Moody’s upgraded Turkey to investment grade (IG) late on May 16.

You probably already know that credit rating agency Moody’s upgraded Turkey to investment grade (IG) late on May 16.