The Central Bank’s Janissary walk

The Central Bank of Turkey

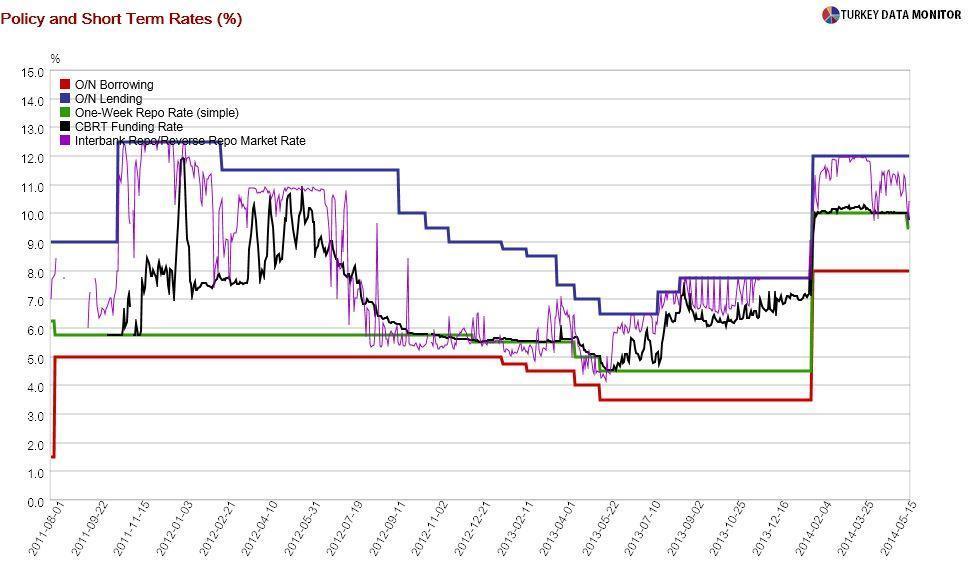

managed to surprise again by cutting its policy (one-week repo) rate from 10 to 9.5 percent, in its latest monetary policy committee meeting on May 22.

It was not a complete shocker. Five out of the 19 economists surveyed by business channel CNBC-e were expecting a cut in the overnight lending rate, which is what the Bank has been calling the marginal funding rate to confuse those of us who are not “borderline geniuses,” as a market economist

once described Governor Erdem Başçı.

However, only three economists were expecting a cut in the one-week repo, partly because the Bank had signaled it was returning to traditional monetary policy after its

emergency hike at the end of January. Last week’s rate cut is a step in the opposite direction, but I am used to a

Janissary walk from the Central Bank: Two steps forward, one step back.

In the

one-pager accompanying the rate decision, the Bank gave the fall in market interest rates across all maturities, due to the “recent decline in uncertainties and improvement in the risk premium indicators”, as the reason behind the rate cut. Bank officials had been

emphasizing the fall in Turkey’s credit default swap spreads. I guess they were paving the ground for the cut.

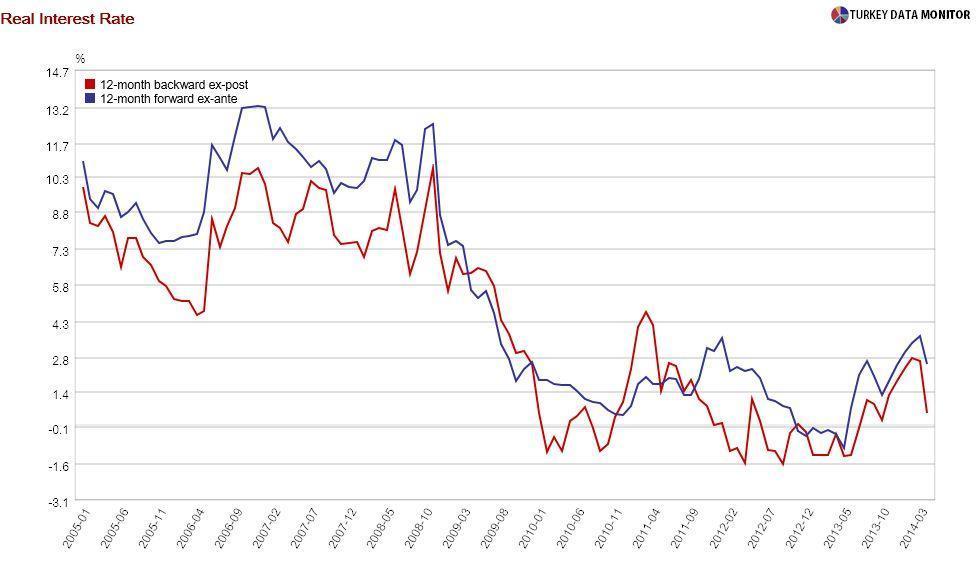

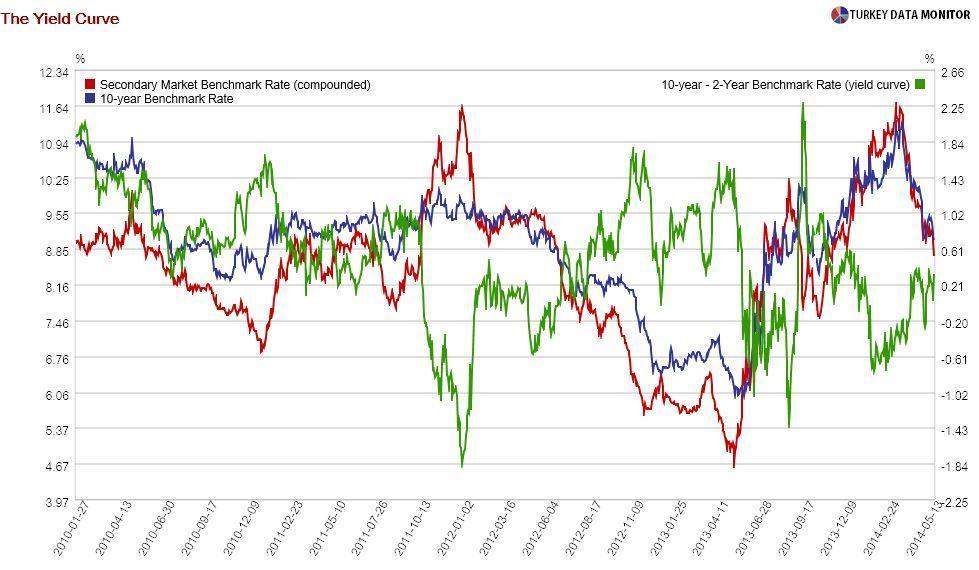

According to the Bank, the monetary policy stance is still tight despite the rate cut (and nearly zero real interest rate) because we have “a flat yield curve even after this decision.” In a way, the Bank is saying “don’t believe what I do, believe what I say.”

More generally, market interest rates have now officially become an integral part of both the Central Bank’s objective function, which is traditionally reserved for growth, inflation (and maybe financial stability) and monetary policy goals. The Bank may have become the world’s first “yield curve targeter.”

Joking aside, I have serious reservations about a monetary policy framework that is so much based on markets. Didn’t Bob Shiller just

win the Nobel Prize for showing that markets are not always right? What if markets are like my nephew Demir: They could be crying (rallying) because they think the Bank will give them what they want that way? It is worth mentioning that the recent rally in Turkish assets has not been caused by capital inflows, which have so far been meager.

And if the Bank is so obsessed with markets, what would they make of the

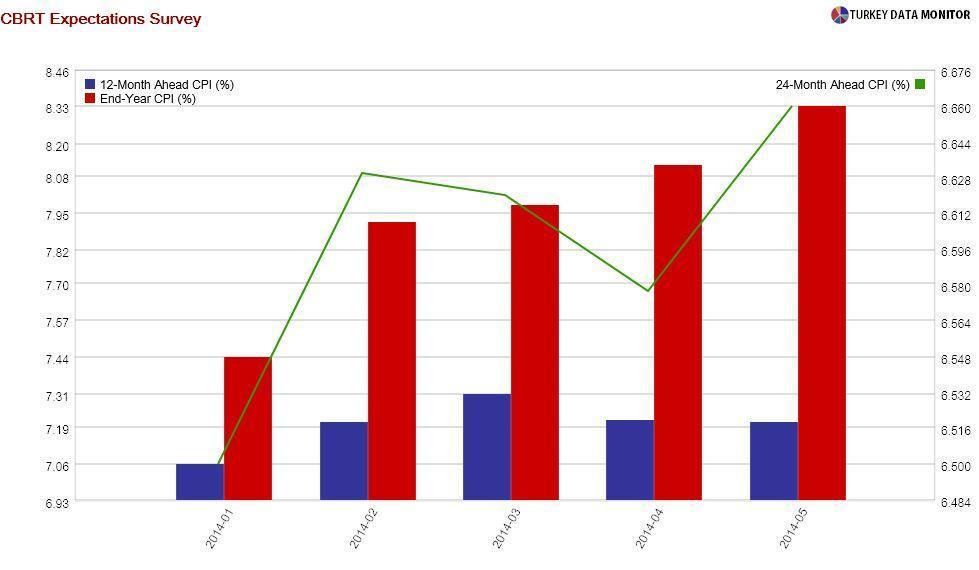

Treasury’s latest auctions on May 20? There was significant demand for the inflation-indexed government bond, hinting that markets are worried about the inflation outlook. Inflation expectations in the Bank’s own survey are continuing to edge up. But don’t worry: The Bank also said in the one-pager that inflation expectations would be closely monitored.

Last but not the least, the Bank chose not to wait to see if the European Central Bank would engage in quantitative easing in its June meeting.

My blog’s host, Nouriel Roubini,

thinks it will not.

The last time the Central Bank trusted Europe in 2011,

it did not end well. Let’s keep our fingers crossed.

The Central Bank of Turkey managed to surprise again by cutting its policy (one-week repo) rate from 10 to 9.5 percent, in its latest monetary policy committee meeting on May 22.

The Central Bank of Turkey managed to surprise again by cutting its policy (one-week repo) rate from 10 to 9.5 percent, in its latest monetary policy committee meeting on May 22.