Rate decision leaks from the Central Bank

There was

a huge uproar when the Turkish Statistical Institute released November inflation figures

17 minutes early by accident exactly two weeks ago. No one reacted when Central Bank of Turkey Gov. Erdem Başçı revealed tomorrow’s rate-setting decision a week early.

I am of course joking. While Başçı,

speaking in Antalya on Dec. 11, implied that the policy rate (one-week repo) and the floor of the interest rate corridor (overnight borrowing rate) would be cut on Dec. 18, he was under no obligation to do so. However, according to Halkbank head of research Işık Ökte, who was

quoted by Bloomberg, “everyone’s grandmother knows Başçı will be cutting.”

In fact, there is still some uncertainty regarding the bank’s moves tomorrow: While all but one of the 16 economists surveyed by business channel CNBC-e expect a cut in both the policy and overnight borrowing rates, four believe the bank will lower the ceiling of the corridor (overnight lending rate) as well.

For once, I agree with the consensus, but for different reasons altogether. Most economists are basing their decisions not only on Başçı’s comments, but also on last week’s weak growth and industrial production figures. However, as I argued

in my Dec. 14 column, industrial production came in low mainly because of fewer working days, and leading indicators of growth are hinting at a recovery this quarter. Başçı made similar remarks during his Antalya speech, noting that “double-digit industrial production is possible in November.”

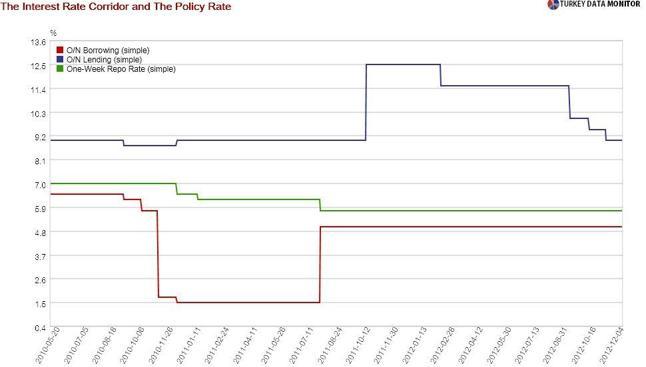

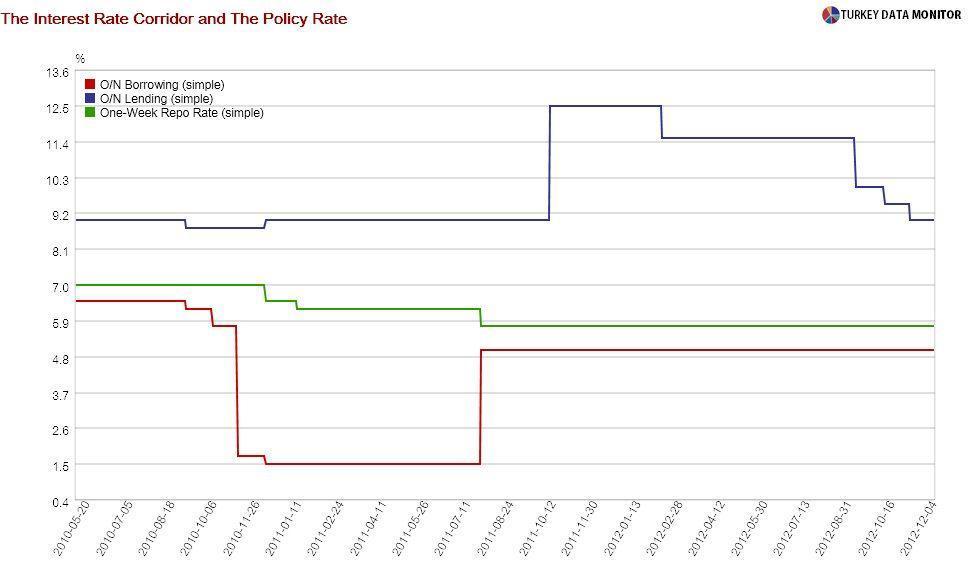

So then why is the bank going to lower interest rates tomorrow? The cut in the overnight borrowing rate should not be a shocker: After all, the Federal Reserve’s (Fed)

decision last week to buy $45 billion of bonds each month and commit to low rates as long as unemployment stays above 6.5 percent and inflation below 2.5 percent should encourage capital flows to emerging markets. The bank responded to such flows at the end of 2010 by widening the corridor and creating interest rate volatility to deter hot money.

As for the policy rate cut, the governor reiterated in Antalya his earlier remarks that a level above 120 for the real effective exchange rate (REER) would warrant a cut. Since the REER was around 119 in November, the bank is either calculating it on a day-to-day basis or expecting strong capital flows because of the Fed’s move.

In any case, I have serious reservations about targeting the exchange rate so openly. If nothing else, such an approach could end up transforming REER into an anchor for monetary policy that would take precedence over inflation. Besides, it could damage the bank’s credibility, as Başçı underlined many times last year that they don’t have an exchange rate target.

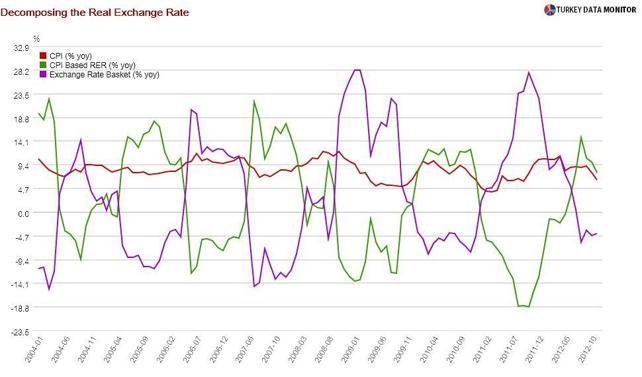

If the bank is really worried about the real exchange rate, bringing down inflation would be a good start. After all, as I showed

in my Nov. 16 column, most of the recent real appreciation is due to the inflation differential between Turkey and its peers rather than an overvalued lira.

There was a huge uproar when the Turkish Statistical Institute released November inflation figures 17 minutes early by accident exactly two weeks ago. No one reacted when Central Bank of Turkey Gov. Erdem Başçı revealed tomorrow’s rate-setting decision a week early.

There was a huge uproar when the Turkish Statistical Institute released November inflation figures 17 minutes early by accident exactly two weeks ago. No one reacted when Central Bank of Turkey Gov. Erdem Başçı revealed tomorrow’s rate-setting decision a week early.