May presenting trouble for Turkish economy

Mustafa Sönmez - mustafasnmz@hotmail.com

While the month of May is a joyful month for emerging countries that have been seeing the bright sun since February, fall winds have begun to blow in Turkey’s economy.

The reason for this is the disturbance in domestic politics. President Recep Tayyip Erdoğan, who is focused on the transition to the presidential system, suggested to Prime Minister Ahmet Davutoğlu that he quit amid differences. The markets subsequently fluctuated, and this course is expected to continue until and after a ruling Justice and Development Party (AKP) convention on May 22.

This turbulence has manifested itself in an increase in the dollar/Turkish Lira exchange rate, which had been decreasing since February. Turkey’s risk premium increased and, consequently, portfolio investments decreased amid occasional capital withdrawals. This fluctuation was reflected in the reports of international credit rating agencies and affected investment intentions. This autumn atmosphere was further affected by Erdoğan’s comments straining the refugee talks with the European Union.

The project to associate a visa-free travel for Turkish citizens with Turkey’s democratization charted a path for stormy waters with Erdoğan’s words, “You go your way; we’ll go ours.” The consequence of this was a distancing from the EU anchor, which discouraged investments in Turkey.

Political turmoil With Turkey’s political turmoil coinciding with the international sales wave, the Turkish markets encountered high turbulence in May. In the second week of May, the turbulence seemed to decrease but it inflicted a certain amount of damage.

The development that triggered the global turbulence was the devaluation of the dollar, which increased the prices of assets in a short time. Investors opted to sell to make profits.

As a result of a number of reasons, the main factor of which was the indecisiveness of the U.S. Central Bank Fed on rate hikes, the dollar index which was 99.000 in February went down to 91.000 on May 3. It recovered in the following three days and came close to 94.000. But the exchange rates of developing countries lost 19 percent of their value after gaining 10 percent against the dollar amid the latest turbulence.

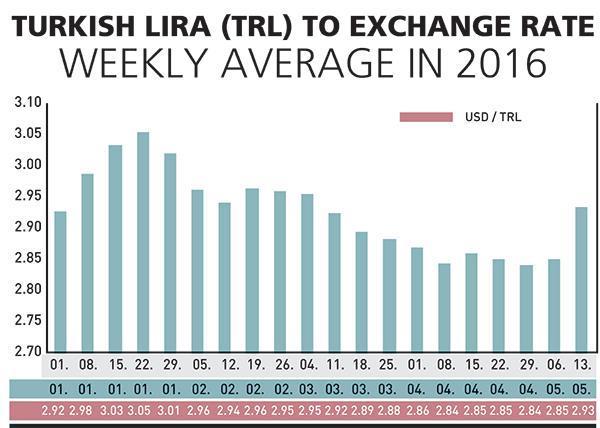

The lira also picked up value, but with the effect of domestic political developments, it again lost value after May 4. In the last week of April, one dollar equaled a weekly average of 2.84 liras, but in the week of the political turmoil and afterward, it leaped to an average of 2.93 liras.

As one would expect, when foreign investors saw the increasing risk and started selling, the fall in the bourse increased.

Risk increase

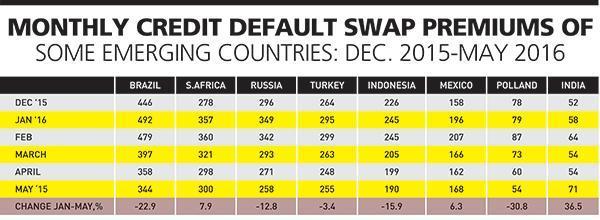

The fluctuation in domestic politics negatively affected Turkey’s risk premium, the credit swap default (CDS), and the April average of 248 went up to 255 in the first week of May, increasing 3 percent. Meanwhile, Brazil’s risk decreased 4 percent in the first week of May. Also, Russia’s decreased 4.8 percent, almost reaching Turkey’s risk premium. One of the fragile five, Indonesia, saw its risk premium also decrease 5 percent during the same time frame. There was not much change either in South Africa.

How will May end and what will happen afterward? The answer to these questions will be determined by domestic and international factors. The non-agricultural employment data of the United States released on May 6 was weak, further decreasing the possibility of the Fed hiking rates in June. This new situation is at least expected to stop the increase in the climb of the dollar’s value.

The domestic political uncertainty peaked on the evening of May 4 when Prime Minister Ahmet Davutoğlu’s news of his resignation came, but the realization that this matter would not go all the way to a political fight and effect an inner-party split decreased the uncertainty. When the date of the party convention was moved to the closest date possible, the strength of the turbulence was lessened.

It is expected that a major section of this uncertainty will end on May 22. But you never quite know what the days will bring. The expectation is that only one candidate will run for office in the AKP convention and that one candidate will be elected as party chair. Will all developments happen as expected? This is unclear.

The future of the economic administration is also significant. However, once the prime ministerial candidate is known, the economic management will also become clear. The dose of political uncertainty is also dependent on whether the party convention of the Nationalist Movement Party (MHP) will be held or not. Any renewal in the MHP may be important for the AKP and for the date of any elections. This is at least how the financial markets perceive the situation.

Credit rating

It will be important to maintain the investable credit rating during this period of transformation and turbulence. International ratings agency Moody’s has maintained a negative outlook for Turkey for two years, while JP Morgan has advised a lowering of positions in Turkish assets. If Moody’s lowers its rating, then Turkey would be lacking an investible rating category from two of the three major agencies. It is not sufficient to secure the assent of only one of the major agencies to remain in the investable category.

Standard & Poor’s, which is known for its critical stance on Turkey and which has given a rating below investment level, provided hope with its evaluation last week. While Turkey’s credit note remained BB+, its outlook was changed from negative to stable. One notch above that is the “investable country” position.

S&P’s cited the resilience of the Turkish economy in the face of global and local threats to the country’s stability, saying the economy still faced challenges ranging from political turbulence to a Kurdish separatist conflict and geopolitical risks from the war in neighboring Syria. “The stable outlook reflects our expectation that Turkey’s economic growth prospects will remain resilient to external shocks and domestic political risks.”

In other words, while it was noted that the risk was increasing, it was not only this outlook that was rated but also the resilience to the risk – something on which Turkey has displayed positive indicators.

While the month of May is a joyful month for emerging countries that have been seeing the bright sun since February, fall winds have begun to blow in Turkey’s economy.

While the month of May is a joyful month for emerging countries that have been seeing the bright sun since February, fall winds have begun to blow in Turkey’s economy.