Central Bank’s credibility on the line

Central banking is supposed to be as much about credibility as about hiking or lowering interest rates.

Central banking is supposed to be as much about credibility as about hiking or lowering interest rates.So when a central bank governor dons his or her country’s flag, goes on live TVi and says they will defend the national currency “like lions,” everyone should get the message. But for some strange reason, Central Bank of Turkey Governor Erdem Başçı’s remarks did not have the desired effect for a second time.

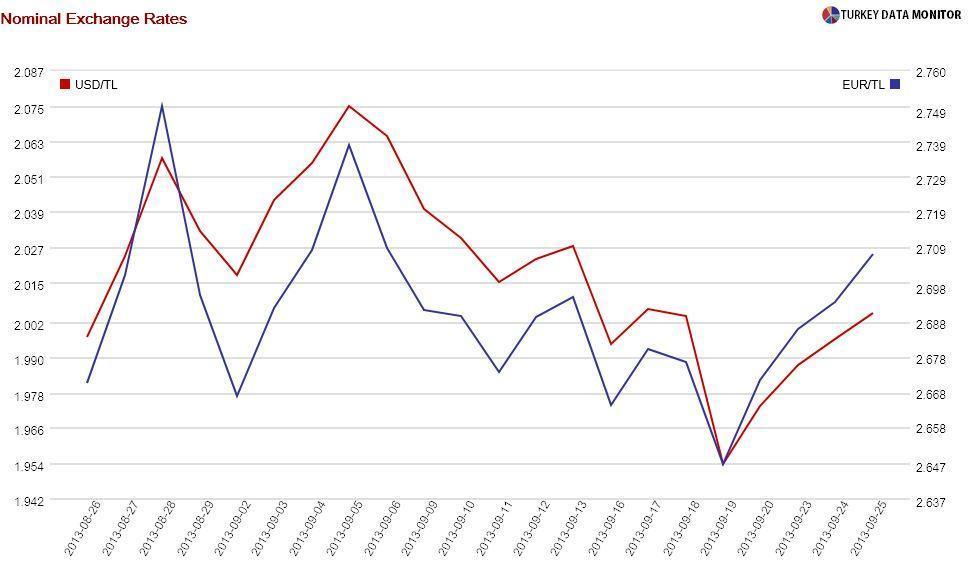

Almost a month after his guarantee of a lira dollar exchange rate of 1.92 at the end of the year, the governor reiterated his promise during a speech in the southwestern town of Denizli on Sept. 24. His remarks led to a sell-off in government bonds, equities and the lira again. I could just tell you that it was because he forgot the flag, or I could give you solid reasons why he and the Central Bank are suffering from what we economists call a credibility gap.

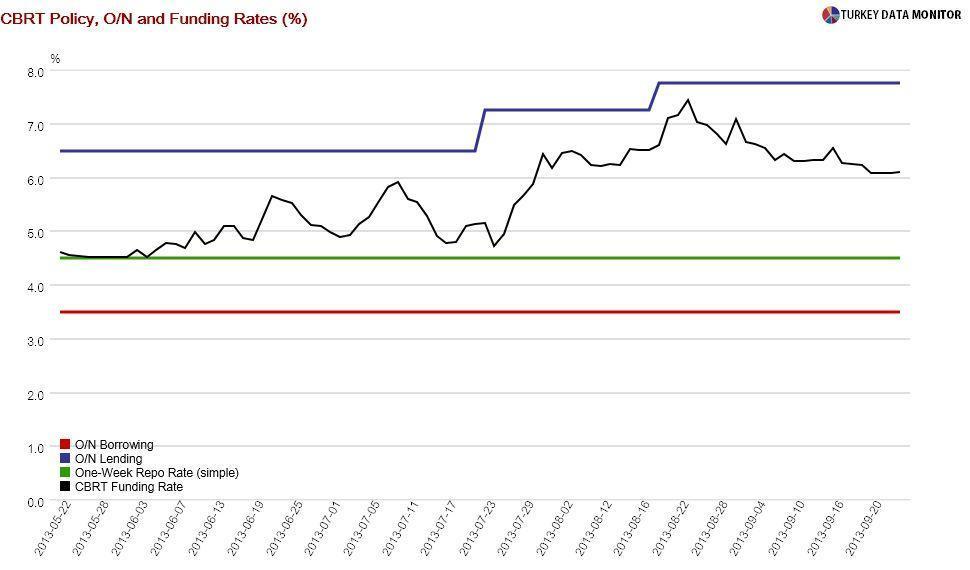

For one thing, although Başçı stated in August that the average funding rate would hover between 6.75 and 7.75 percent until inflation hit the Bank’s year-end forecast of 6.2 percent, it has actually fallen since then. This is because the Bank has funded the markets more and more at the cheaper (4.5 percent) one-week repo. Başçı clarified during his Denizli speech that he was excluding this rate, which is incidentally the policy rate, from the calculation.

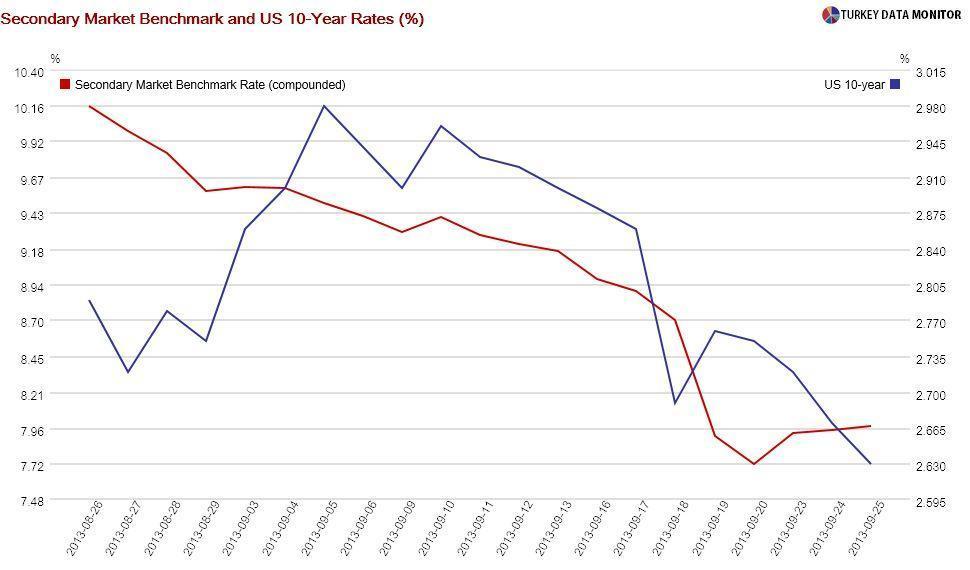

By the way, Başçı confirmed what Turkey economists already knew: The end-year inflation projection will not be reached at the end of the year. According to the governor, the culprit is the recent lira depreciation. If the lira-dollar exchange rate had stayed at the magical 1.92 level, the forecast would have been attainable. But that means the exchange rate pass-through to inflation is higher than the 15 percent he had earlier stated.

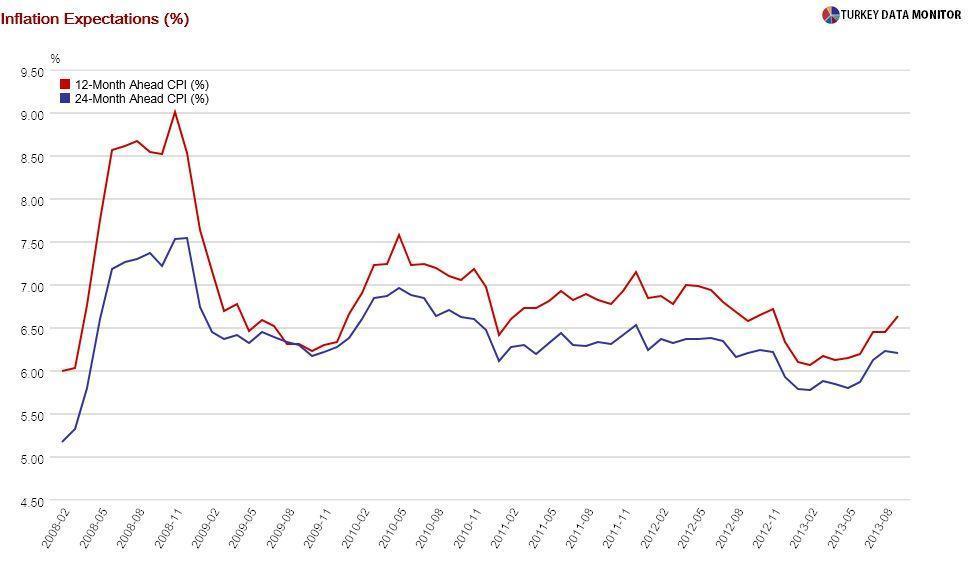

However, you should not expect a response: Başçı said they would increase the policy rate only if the 24-month ahead inflation outlook deteriorates. It has been “conveniently” tame so far, but if it starts to rise, I am sure he will find another excuse not to hike rates. By the way, I am not sure if Başçı’s condition includes overnight lending rates, as I don’t see how a policy rate hike would be effective without an increase in the ceiling of the Bank’s interest rate corridor.

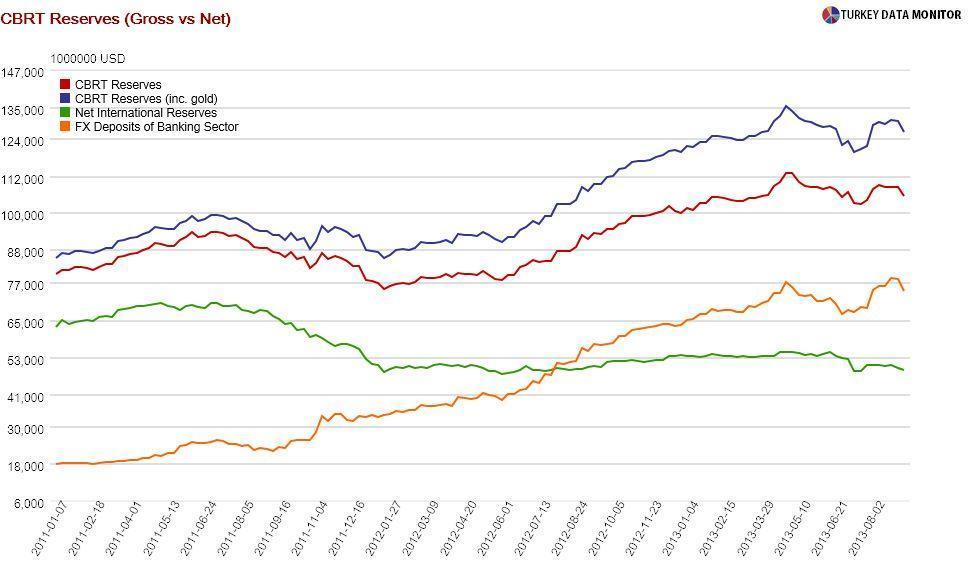

Başçı also revealed in Denizli what I had been suspecting: There is no new monetary policy tool. The “surprise” measure he hinted in August turned out to be good old unsterilized foreign currency (FX) interventions. With net reserves below $50 billion, the Bank’s arsenal is limited. Başçı mentioned they could lower reserve option coefficients and FX reserve requirement ratios as well, but these measures won’t make a big difference.

I would nevertheless expect heavy interventions if the lira-dollar exchange rate gets too far from 1.92. Başçı knows that his and the Central Bank’s credibility, already tarnished by conflicting remarks, will be irreparably destroyed if he can’t keep his FX promise. Then, even the flag won’t help.