Data marathon deceives most

Dec. 11’s October current account deficit did not get much attention, as it was in line with expectations. Markets were also still busy trying to digest the previous day’s disappointing growth and industrial production numbers. However, I am more worried about the deficit than the other two.

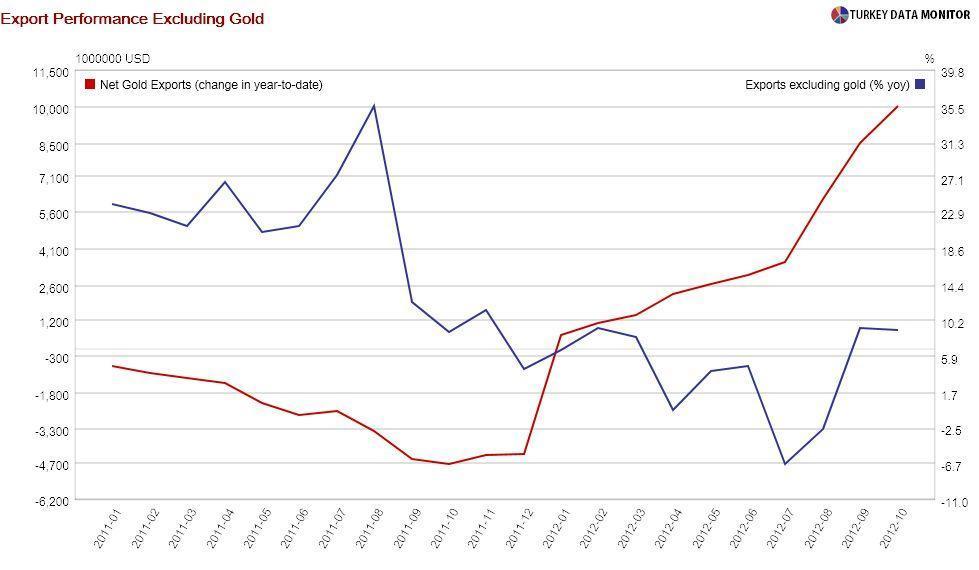

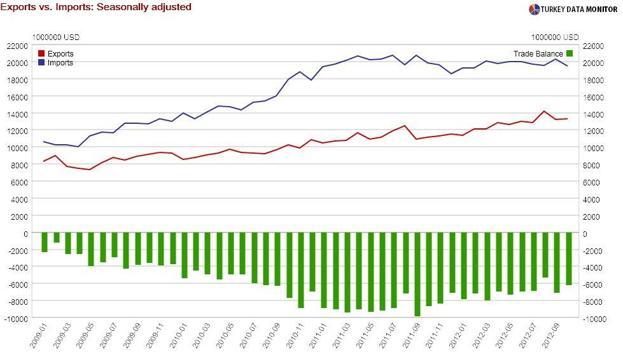

Dec. 11’s October current account deficit did not get much attention, as it was in line with expectations. Markets were also still busy trying to digest the previous day’s disappointing growth and industrial production numbers. However, I am more worried about the deficit than the other two.The current account deficit narrowed by almost $24 billion in the first 10 months of the year compared to the same period last year. This looks like an impressive feat, as exports increased 13 percent and imports fell 2.5 percent. However, $10 billion of this adjustment came from Turkey’s unofficial gold-for-gas program with Iran.

Once you take out gold, export growth turns out to be a less impressive 4 percent. Contrary to what Economy Minister Zafer Çağlayan is claiming, exports are not the driving force behind the current account adjustment. The plunge in imports is at least equally important.

Seasonally adjusted data hint this adjustment may have come to an end. As I argued in Dec. 7’s column, leading indicators for exports are painting a bleak picture for the next few months. Moreover, it also seems imports are still sensitive to growth. Therefore, I would not be surprised if the current account deficit starts widening again in the first half of the year once growth picks up and gold exports to Iran stall.

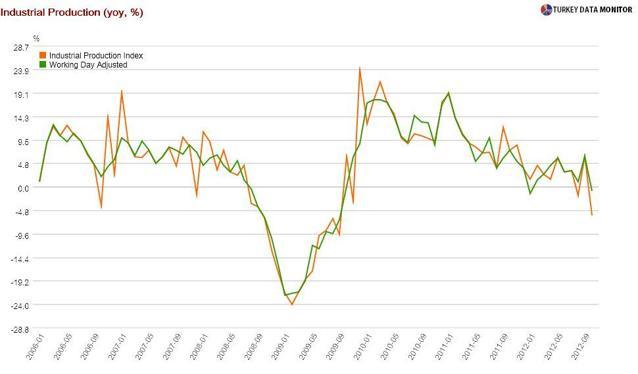

Of course, for anyone following the Turkish economy closely, my economic recovery assumption will probably seem a bit far-fetched at the moment. After all, both third-quarter growth and October industrial production disappointed on Dec. 10.

While the yearly drop in industrial production was much more than expected (5.7 versus 2.5 percent), these data are notoriously volatile, and so a strong pickup next month would not surprise me. Besides, part of the sharp fall is due to fewer working days in October compared to the same month last year because of the Feast of Sacrifice holiday. Once you adjust for working days, the yearly decrease becomes a mere 0.9 percent.

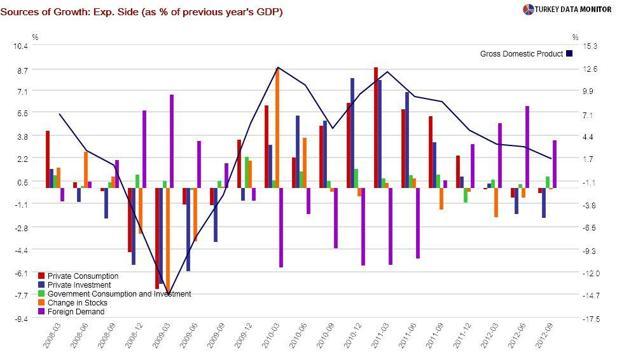

As for gross domestic product, the lower-than-expected turnout of 1.6 percent (versus expectations of 2.5 percent) was mainly due to private investment, which decreased 11.2 percent yearly and shaved off 2.2 percent from growth, although the contribution of net exports was also less than predicted, and private consumption lowered growth by 0.4 percent.

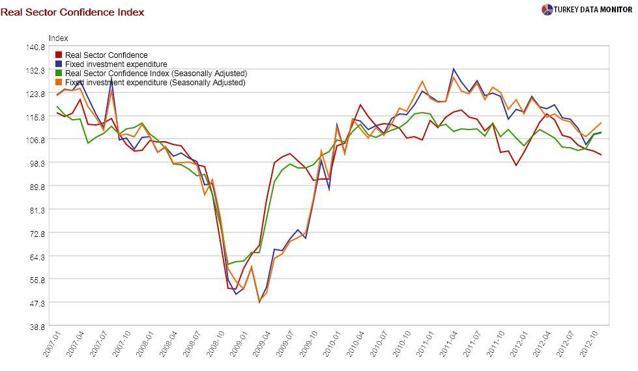

The same leading indicators, such as the Purchasing Managers’ and Real Sector Confidence indexes, that are hinting a slowdown in exports are also foretelling a pickup in investment. The real question is whether the consumer will keep pace, as leading indicators of consumption are pointing to subdued demand. After all, if exports turn out to be weak as well, firms cannot continue producing into their inventories forever.

My spider senses are telling me that with the ultralow interest rates, consumption will eventually recover. I will tackle this issue in a column titled “O Consumer, Where Art Thou?” in a couple of weeks.