The year of economic surprises

Turkish economic data surprised in 2012. The best way to show that would be to compare expectations of economic variables from the Central Bank’s Survey of Expectations with actual realizations.

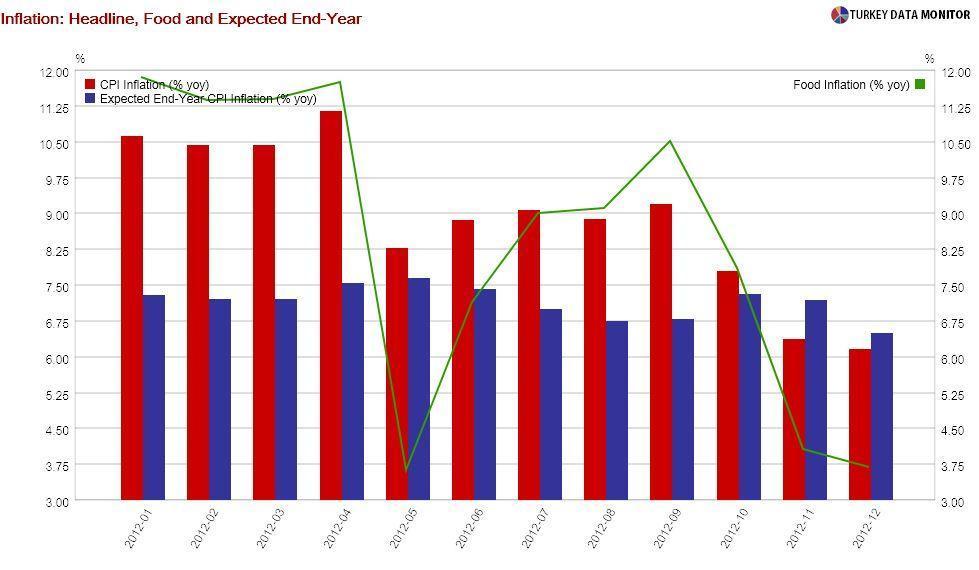

Turkish economic data surprised in 2012. The best way to show that would be to compare expectations of economic variables from the Central Bank’s Survey of Expectations with actual realizations.The big economic theme of the year was “adjustment.” We started 2012 with an inflation of 10.5 percent and current account deficit of $77 billion. With yesterday’s December figure, inflation ended the year at 6.2 percent, and the deficit is $53 billion as of October.

With the Central Bank’s sharp tightening in the last quarter of 2011 and comments from officials on the need to slow down the economy, everyone was expecting some improvement in these two variables. For example, in the first three months of the year, year-end expectations were around 7.2 percent, although actual inflation was in double-digit territory.

But no one was expecting such a low figure. The government’s own projection was 7.4 percent in October, and expectations were still 7.2 percent at the end of November. But it is important not to get carried away. After all, the plunge in notoriously volatile food prices in the last quarter caused the favorable turnout. Besides, this week’s tobacco tax hikes alone are likely to increase inflation by slightly less than 1 percentage point.

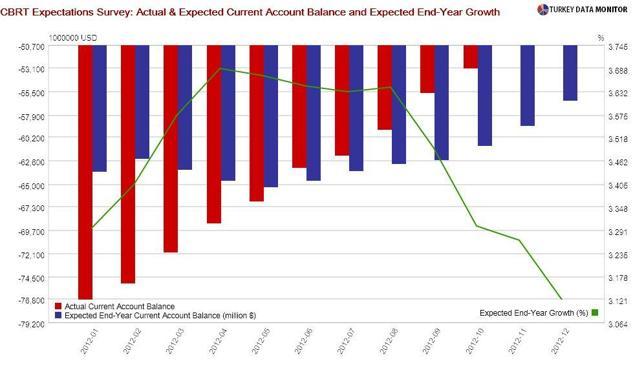

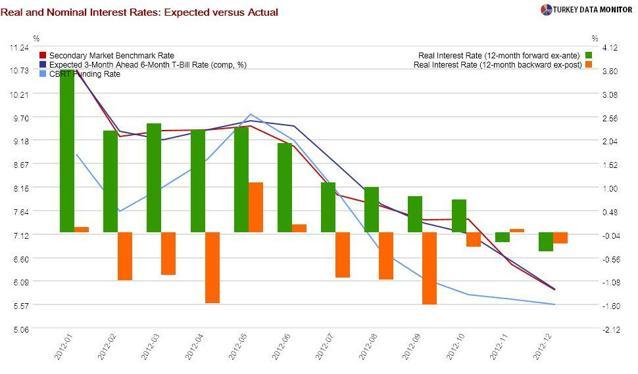

The discrepancy between expectations and realizations is even wider for the current account. The end-year deficit was projected to be just short of $65 billion early in the year. It will likely end up slightly below $55 billion when the December figure is released in February. However, since the trade deficit would have been $10 billion larger without gold exports to Iran, forecasters have not actually been off the mark.

The collapse in the current account deficit can also be attributed in part to the decrease in growth, which is likely to fall to below 3 percent, quite a bit lower than expected, in 2012 after 2011’s eye-stunning 8.5 percent. Therefore, the current account adjustment seems to be much more cyclical and one-off than structural and lasting.

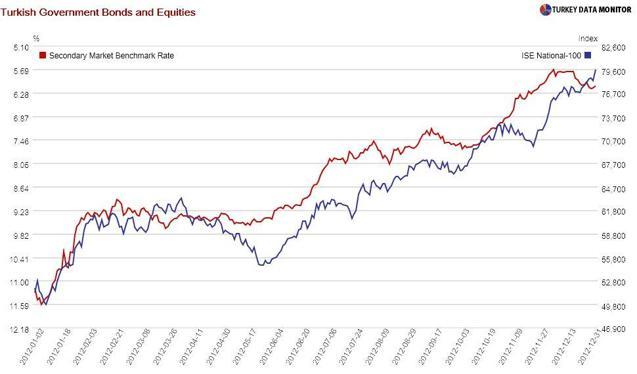

Turkish asset prices surprised even more than macroeconomic variables, with equities and bonds hitting record levels. While the European Central Bank’s Outright Monetary Transactions in July and the Federal Reserve’s Quantitative Easing 3 and 4 in September and December were game-changers, Turkey had a couple of specific factors going for it as well.

One was the Central Bank, which started easing monetary policy, unexpectedly and aggressively, in the summer. It also helped that the Bank had eliminated currency risk by effectively fixing the exchange rate. And once the country got the much-longed for investment grade from ratings agency Fitch, nothing could hold Turkish equities and bonds back.

In sharp contrast to how it started, 2012 turned out to be a good year for Turkey. Since all’s well that ends well, I should not be too worried. But I can’t help it; worrying is in my nature. And besides, I have good reasons to be concerned, as I will outline on Monday.