The Fed interest rate that came with the winter chill

Mustafa Sönmez - mustafasnmz@hotmail.com

FILE _ In this Wednesday, Dec. 16, 2015 file photo, specialist Edward Loggie works at his post on the floor of the New York Stock Exchange as the rate decision of the Federal Reserve is announced. The Fed's move to lift its key rate by a quarter-point to a range of 0.25 percent to 0.5 percent ended an extraordinary seven-year period of near-zero rates that began in the depths of the 2008 financial crisis. (AP Photo/Richard Drew, File)

It was 2.5 years ago, in mid-2013, that then-U.S. Central Bank Fed Chair Ben Bernanke gave the signal that interest rates would be increased. His successor, Janet Yellen, finally did what needed to be done. The Fed ended its zero interest rate policy after seven years and started its rate hike with 0.25 points. It was a widely anticipated interest rate hike that had allowed the entire world to prepare in the meantime.With the global crisis, the Fed gave a lifesaver to the market to prevent the rapidly shrinking economy from causing further damage with its monetary expansion policy. As a result, its balance sheet increased to $4.5 trillion from $925 billion with this intervention.

With these measures, the economy’s bottoming out was slowed down and the Fed began giving signals that it was going to remove this crutch and that everybody should be able to stand on their feet according to market conditions. Bond buying and liquidity expansion operations were to decrease gradually and end by October 2014. From that day on, markets began expecting a rate increase. This expectation finally ended on Dec. 16 and the rate hikes began.

Yellen, in her speech, gave a road map for the future and disclosed the route of the rate hikes. According to that, the Fed will gradually increase interest rates depending on how the economy evolves. According to the road map, at the end of 2016, the interest rate will be 1.4 percent. These hikes will continue in 2017 and at the end of 2017, they will rise to 2.75 percent.

Let’s look at the possible effects of this new era on the United States, the developed capitalist countries and the rest of the world.

At the center

Obviously, the rate hike in the U.S. will cause global resources and funds to further flow to the dollar and the U.S. This means that the dollar will again gain value against other currencies.

The capital that will flow to the dollar and the U.S. is the capital that was temporarily parked in countries like Turkey. Thus, with the decreasing of the dollar from these temporary parking spots, the dollar will become scarce and its price will again rise. Local currencies, as they have until now against the dollar, will from now on continue to lose value. The world has been experiencing this regardless since mid-2013. In other words, since then, global funds have started changing positions and slowly reorienting toward the U.S.

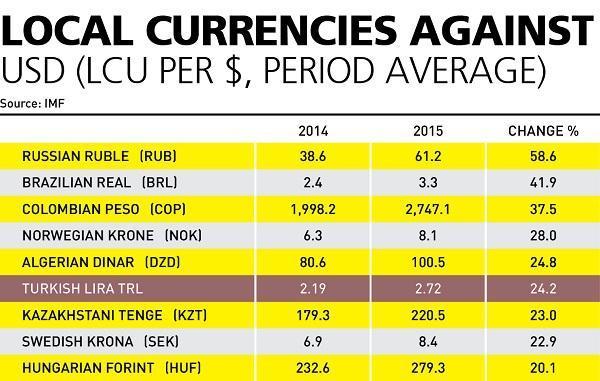

As a matter of fact, according to the IMF database, since the middle of 2013, among the “emerging countries,” the currencies of Russia, Brazil, South Africa and Turkey have lost the most value against the dollar.

If we exclude Iran, particularly because of the sharp devaluation of 102 percent it went through in 2013, then the Russian ruble takes first place in terms of devaluation over the past 2.5 years at nearly 146 percent. This fall, the Ukraine-Crimea crisis and the fall in energy prices also had an impact, in addition to the Fed’s actions.

Again, in the same period, the close to 95 percent devaluation of the Brazilian real had an impact in the drop in the raw materials exported to China. The South African rand was devaluated almost 68 percent, while Turkey’s drop reached 60 percent. The Turkish Lira, especially in 2015, experienced significant depreciations against the dollar.

The local currencies of other emerging countries such as Indonesia and Mexico experienced 40 to 44 percent devaluations over the period in question. In the local currencies of emerging European countries, on the other hand, lesser deprecations were observed. The devaluations of Hungarian, Polish and Czech currencies ranged between 25 and 29 percent. In the same period, the Indian rupee devaluated by 24 percent.

In the U.S.

The rate hike in the U.S. will also activate the country domestically. Companies that have become accustomed to zero interest rates will experience harmonization issues against the increased price in the currency, meaning there will inevitably be some elimination. Some companies and banks will survive or will fall.

The valuation in the dollar will disturb exports, and this, in turn, will cause closings, sales and bankruptcies. In other words, this decision may stir also U.S. capitalism. It will have political and social consequences as well as economic ones.

The central banks of metropolises that move in concert with the Fed after the global crisis will have difficulty making a decision. While the Fed is hiking rates, will the European Central Bank (ECB), China and Japan continue their low interest rate policies? Will the ECB in particular continue expansionary policies? Or will it resort to “wait and see?” The Fed’s decision will shake the EU as well.

The periphery

In the world capitalism equation, there is China’s situation as a prominent variable. China, whose growth has skidded by decreasing its demand on raw material supplier countries, has shaken them. Brazil and South Africa have been especially affected by this fall in demand.

It is also unclear how the low course of oil and commodity prices will react to the new conditions. This will closely affect peripheral economies. Geopolitical risks such as political risks in the Middle East, Islamic State of Iraq and the Levant (ISIL) terror and issues in the South China Sea should also be added to these. All of these uncertainties will provide a hard time for countries like Turkey.

Turkey

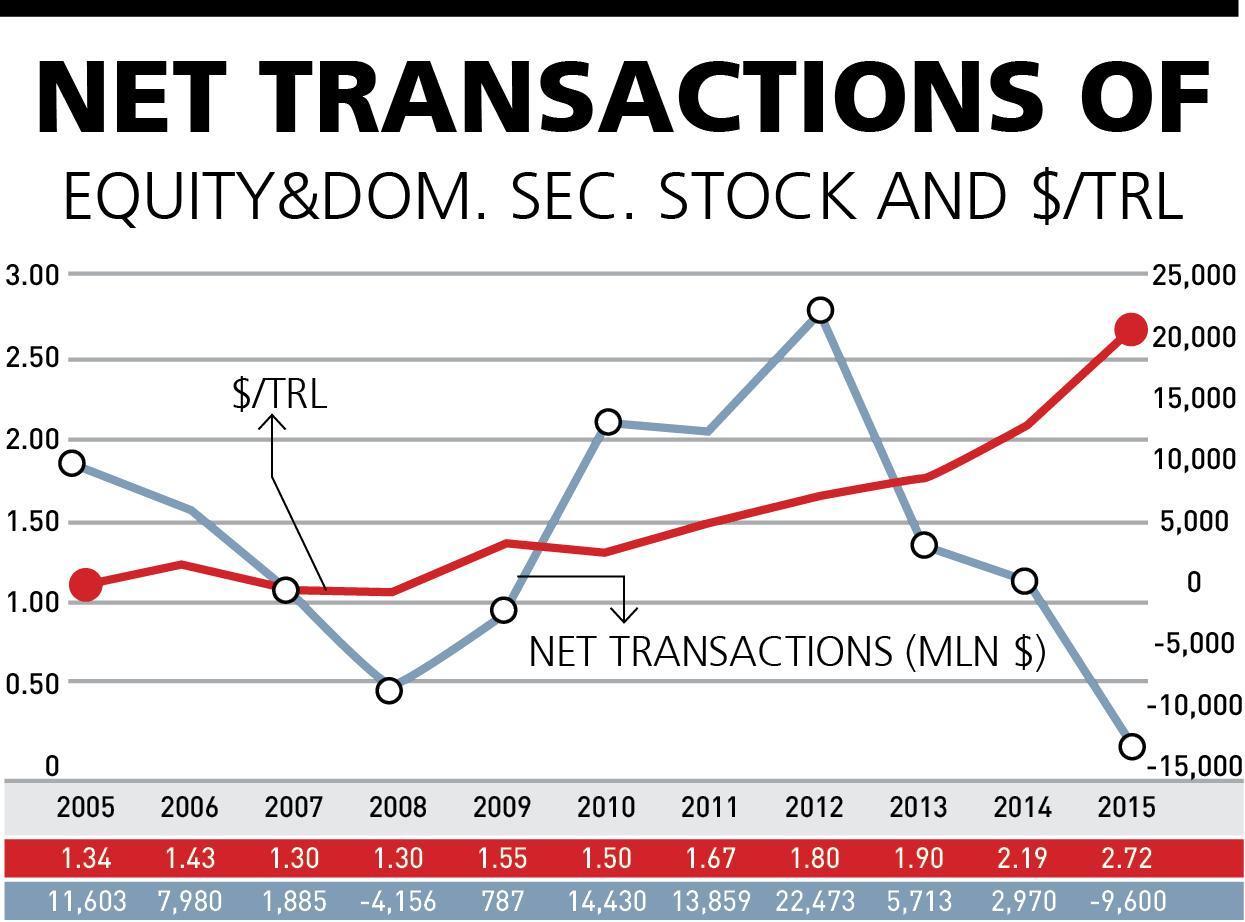

The Fed rate hike variable has been on Turkey’s agenda since mid-2013, like many other periphery countries. The dollar/lira average of 2012 was 1.80 liras; it started climbing in mid-2013. In 2013 this average was 1.90 and a devaluation of 5.5 percent was experienced. This falling trend continued in 2014, and the yearly average of one dollar was 2.19 liras.

The same situation continued in 2015. Net capital withdrawal reached $9 billion throughout 2015. With this effect, there were times when the dollar climbed to 3.07 liras. With the Fed interest rate statements, the dollar neared the 2.90 band, and it looks as if its 2015 average will be 2.70 liras, representing a loss of more than 23 percent.

Risks

The lack of appetite in foreign capital, which has caused a 60 percent loss in value against the dollar in the past 2.5 years, cannot be explained by the Fed interest rate alone. The political and geopolitical risks in Turkey that have accumulated since that date have to be remembered. In 2013, the June-Gezi resistance and the Dec. 17-25 corruption claims increased the country’s risk.

The products of the foreign policy pursued have elevated the country’s risks. Holding four elections in two years naturally made foreigners go into a “wait and see” phase. Even though the AKP has overcome the latest election turn, the season for the Turkish economy is no longer spring, it is the beginning of a long winter.

The increased Fed rate is negatively affecting and will affect foreign capital inflow into Turkey, as in all periphery-emerging countries. Even though Turkey has showcased the advantages of its single-party rule, this is not enough to attract foreigners. Because Turkey, in the eyes of foreigners, is a country that is experiencing domestic tension and clashes, that is pursuing adventures in the Middle East, clashing with Russians, Iran, Baghdad and Syria, is exposed to an economic embargo and is under new threats. The creeping civil war in its southeast is also about to escalate.

The attraction of investing in such a country is fading every day. The best point about the country is its 3 percent annual growth, but there are several more dark clouds over it.

Unless domestic peace arrives in the country, the rule of law dominates, and the search for cross-border adventures are eliminated, then risks will not decrease. Such issues are unlikely to escape the attention of international rating agencies.