Tchau Tchau Inflation Targeting

I may have hurried a bit when I declared in my last column that Turkey, unlike Brazil, did not have to worry about stagflation, the combination of low growth and high inflation.

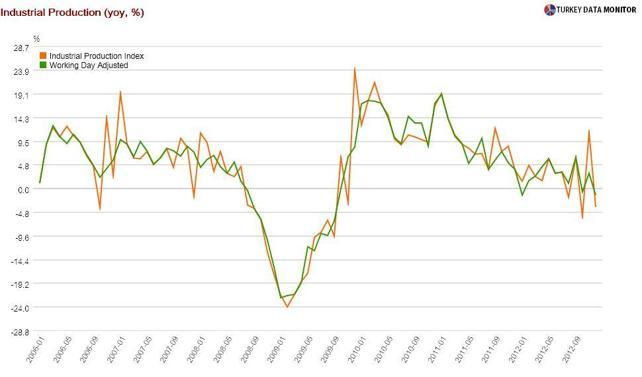

I may have hurried a bit when I declared in my last column that Turkey, unlike Brazil, did not have to worry about stagflation, the combination of low growth and high inflation. December industrial production, which was released on Feb. 8, disappointed. While economists were expecting the index to stay more or less flat year-on-year (compared to the same month of the previous year), it contracted 3.7 percent.

The index is notoriously volatile. For example, it jumped 11.3 percent year-on-year in November after contracting 5.7 percent in October. The wild swings in these two months were due to the big changes in the number of working days compared to the same months of 2011 because of the Feast of the Sacrifice holiday, which drifts approximately 11 days earlier each year.

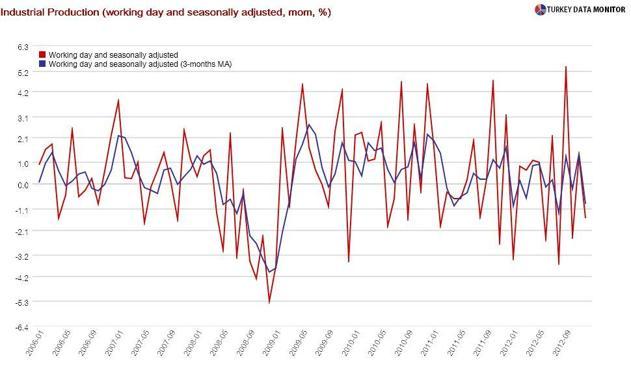

Even without this holiday effect, the number of working days change from month to month and even between the same months. There is also some seasonality in industrial production. However, the Turkish Statistical Institute also publishes a “working day and seasonally adjusted index” that takes these effects into consideration. That index was 1.5 percent lower than in November.

These figures leave the government and the Central Bank in a bind: What is the best way to respond when the economy is not growing as expected, but there are still inflationary pressures? Since Brazil has been suffering from stagflation, the extreme case of this phenomenon, looking at how they are tackling the problem may be helpful.

While Turkey is not threatened by stagflation, economic indicators released in the two countries this month have been telling similar stories. As I discussed in my last column, inflation came in higher than expected in both countries last week. Interestingly enough, the dismal figures were driven by food prices.

Similarly, industrial production in Brazil, released by the Brazilian Institute of Geography and Statistics on Feb. 1, decreased 3.6 percent year-on-year in December. For the whole year, the index fell 2.7 percent. The regional figures released on Feb. 6 point to some pickup in the industrial heartland of São Paulo, but the figures are quite dismal overall.

The Brazilian government chose expansion over inflation. It sent a bill to Congress on Feb. 6 to cut its targeted primary surplus for this year to 1.8 from 3.1 percent of GDP. I would not be surprised if this year’s fiscal targets were breached in Turkey, especially since the country is heading towards a busy elections cycle, with a constitutional referendum on the agenda in addition to the local, presidential and general elections coming up in the next two years.

The more immediate response will come from the Central Bank of Turkey. They would be keener to stimulate the economy by lowering the interest rate corridor, especially if such a move is supported by an appreciated currency. On the other hand, they may be very slow in hiking reserve requirements further.

As for the inflation target, it is tchau tchau, both in Brazil and Turkey.