Sea of risks failing to calm troubled Turkish economy

Mustafa Sönmez - mustafasnmz@hotmail.com

The Central Bank, which is headed by Erdem Başçı, could be affected greatly if the US Fed finally decides to end its liquidity program.

After the Nov. 1 elections, the markets enjoyed tranquility. The fluctuating and swinging mode had given way to a less turbulent climate; it seemed so but then the plane shooting incident erupted with Russia. But again, compared to the pre-election period, it is portrayed as an environment with low uncertainties.Turkey has had an intense uncertainty environment for the past two years. On one hand was the election rush and on the other were two years of turbulence because of changes in external economy policies.

Economy players were exhausted with pessimism at times and short-lived rallies at other times. They opted to avoid risks. In the past month though, these circumstances have changed. It did not disappear totally but uncertainties decreased slightly.

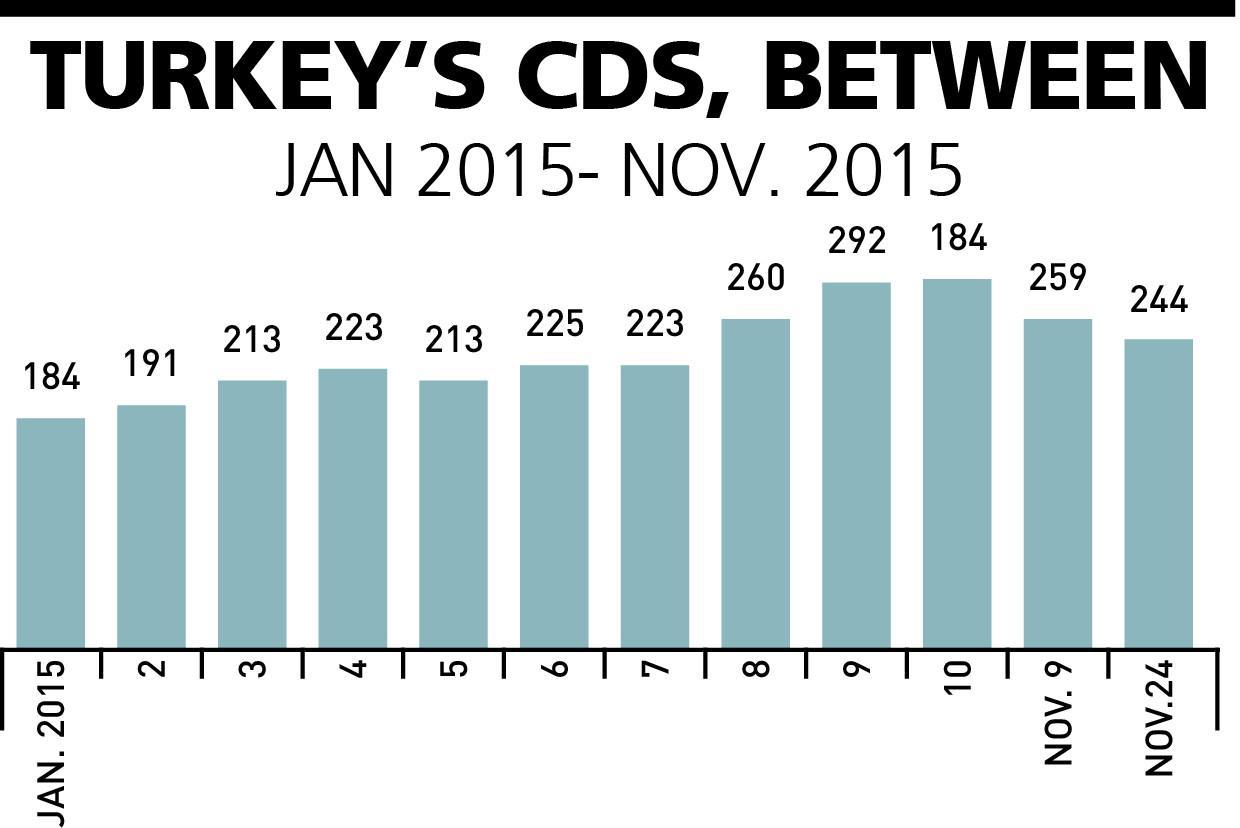

The economic climate seems to have moderated. As a matter of fact, Credit Default Swap (CDS) started to decline for Turkey after the Nov. 1 election. The year started at 184 and continuously increased until mid-October 2015 to 292 then started falling. On Nov. 9, it was 259. On Nov. 24 it was 244. But with the Russian crisis it increased again to 254.

At the top of the factors that created the foggy atmosphere was the political uncertainty created by elections one after the other. During that period Turkey had to run a tough political marathon of local elections, presidential elections and general elections with the unusual repeat of a general election.

Elections always create uncertainty and risk. The question of who will lead the economy after an election creates uncertainty. Players, justifiably, regard this as a risk. If there is a chance of a change of government then this uncertainty intensifies, the perception of risk increases and everybody tries to adjust their positions accordingly.

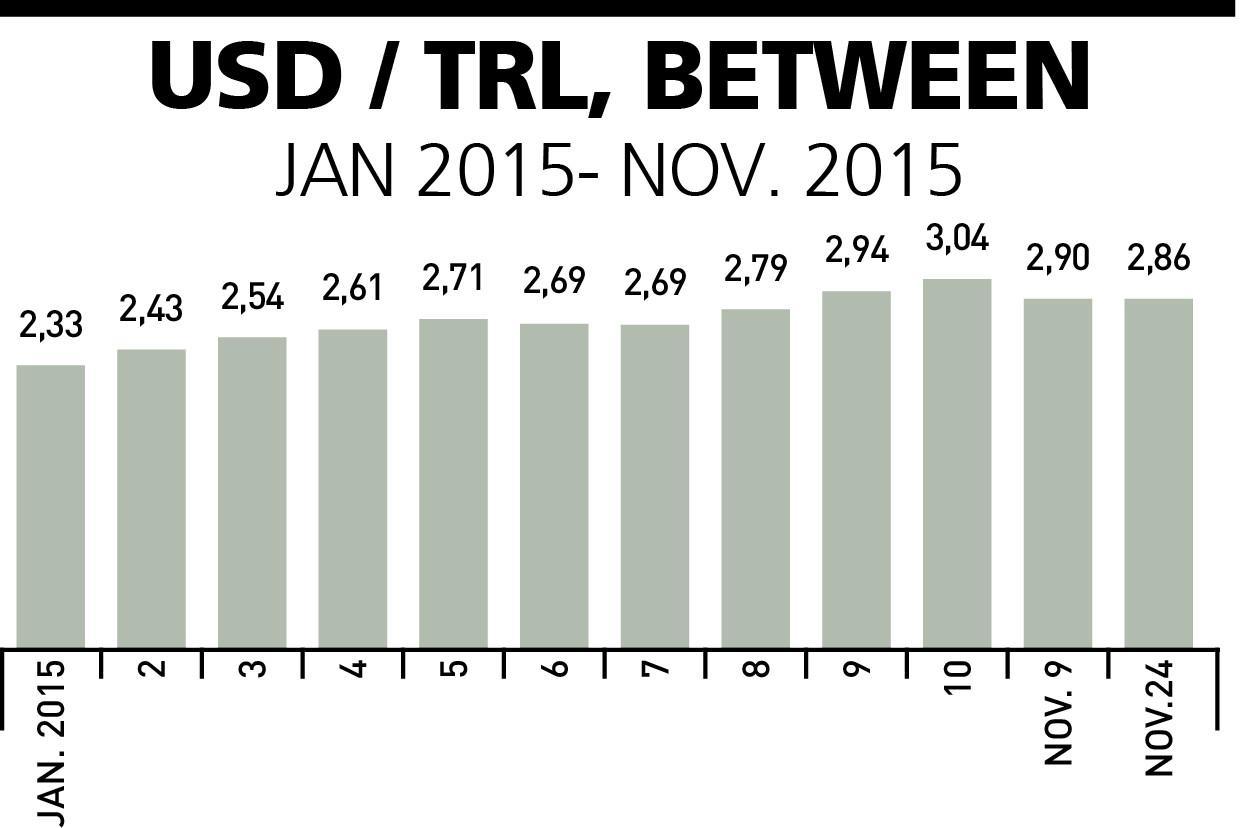

After the Nov. 1 election, the election marathon was over and political uncertainty was decreased to a great extent. The risk perception declined. The results of this immediately showed. For instance, the dollar/Turkish Lira parity fell. The dollar exchange rate, which had gone above 3 liras from time to time, went down to around 2.80 after Nov. 1. It went up a little afterwards depending on international developments. It looks as if foreign dynamics will be more determinant in possible further climbs.

No doubt, advancement on the road to normalization does not mean domestic risk factors are totally eliminated. For instance, geopolitical risks still stand. In this context we can say there is a decline here also. The drift of Islamic State of Iraq and the Levant (ISIL) terror actions to Europe from Turkey at least made the risk of Turkey a shared one. This situation created a moderation in the risk perception of Turkey. However, the downing of the plane crisis with Russia made the climate harsh again. But there is a probability that it may be moderated. On the other hand, clashes with the outlawed Kurdistan Workers’ Party (PKK) are continuing, remaining as a serious risk factor.

The Fed factor

International developments also contributed to the decline of uncertainties. For instance, the American Central Bank (Fed) has given signs that its ongoing vagueness will come to an end and this has helped the risk perception to decline. The fact it is almost certain the Fed will increase rates next month has also brought calculations of who will be affected by this move, how and by how much.

The first findings point out that the effect will be less than anticipated and a much lesser number of countries will be seriously affected. The first outlook seems as if Turkey will not be among these countries but this can be misleading. Some 40 percent of Turkey’s outstanding external debt has to be rolled over in 12 months and there is no noteworthy increase in portfolio investments after Nov.1.

On the other hand, during the Fed rate hike, two important central banks, Europe and Japan, will opt for monetary expansion likely to ease the Fed effect. Even if this is just an impression, we can say that would decrease the tension to a great extent.

These developments are important but they do not mean that the problem is totally solved. The relaxation after the elections has at the same time left the markets without a direction, with the route unclear.

‘Old times’

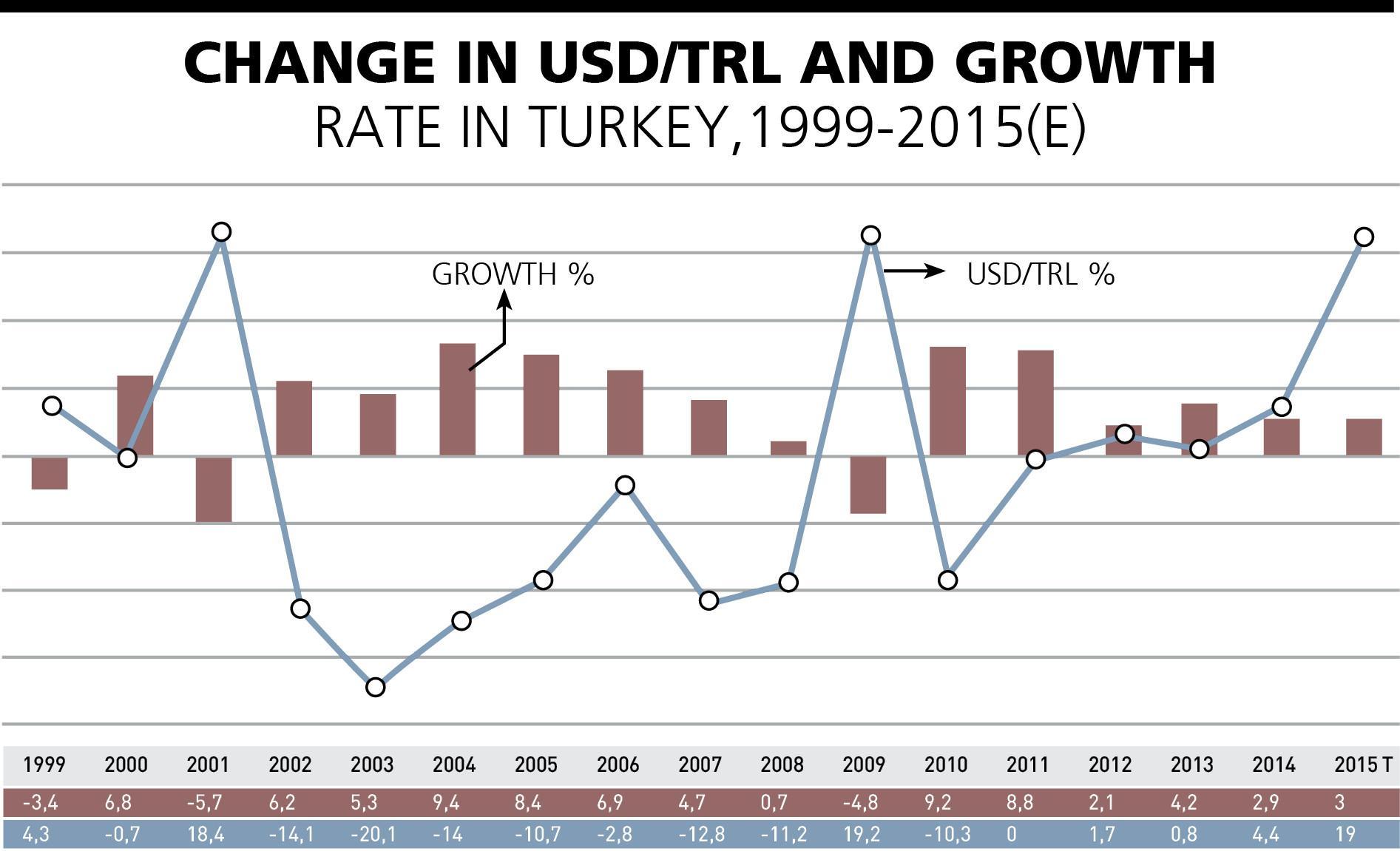

The course of the dollar against the lira has been influential for years in Turkey’s economic growth. In the pre-2001 period when the deepest economic crisis of Turkey was going on, the dollar’s price was almost the same as annual inflation, reaching 60 to 70 percent. This smashed all parameters paving the way to the inevitable 2001 crisis.

With the IMF’s anchor currency recipe failing in 2000, the heavy current account deficit and the exit of foreign investments took the devaluation of the lira against the dollar to 89 percent. This much devaluation brought a historic economic shrinkage of 5 percent and an industrial shrinkage of 9 percent.

The foreign investment inflow after the 2001 crisis made the dollar rate cheaper and the cheap dollar became a wind for economic growth. Between 2002 and 2007 high capital inflow made the dollar rate cheaper, more than 12 percent annually.

This was the rising period of the ruling Justice and Development Party (AKP) and at this time the annual capital inflow averaged at $25 billion. While $19 billion current account deficit was paid, reserves strengthened also. This was a honeymoon period with the dollar rate cheapening at a rate of 12 percent annually, high growth and high imports. Similar climates were experienced in several emerging countries such as Brazil, India, South Africa and many Asian countries.

The effect of the dollar rate on industrial growth was noteworthy in the period between 2003 and 2008. In this period the economy grew at an average of 6 percent annually; then it exceeded the average by 1 point making the annual average 7.1 percent. In the period between 2009 and 2015, the dollar gained value and the annual loss of the lira reached 5 percent. In this period annual average growth fell to 3.5 percent while the average industrial growth fell to around 4 percent.

The cheap foreign exchange rate did not advance exports much but it stimulated imports; while domestically-oriented growth accelerated imports the foreign trade deficit grew every year. When the deficits were not met by foreign currency-generating sectors such as tourism, then current account deficits became Turkey’s chronic problem.

During the second phase of 2009 through 2015, the global crisis was dominant and the dollar exchange rate lost 5 percent annually. The years that pulled this average rate higher were 2009 and 2015 and in each of them the lira lost 19 percent value against the dollar free of inflation.

The dollar exchange rate in 2009 was 1.55 liras. It went up to 2.85 liras in 2015. This nominal increase, when free from inflation, corresponds to an annual loss of 5 percent. Nevertheless, the fact that this devaluation intensified in these two years even though it negatively affected the growth and industrial growth was spread out in time.