‘Should’ monetary policy

On my first day on the job as a market economist in 2006, my boss, an economics Ph.D. who had worked at the World Bank and the Central Bank of Turkey before joining the ranks of finance, pulled me aside to explain the difference between academic and market economists.

On my first day on the job as a market economist in 2006, my boss, an economics Ph.D. who had worked at the World Bank and the Central Bank of Turkey before joining the ranks of finance, pulled me aside to explain the difference between academic and market economists.“Academics tend to spend too much time on what the Central Bank should do. But your clients do not care about that. You need to tell them what the Central Bank will do.” And that I did, with a good forecast record. Not that I had a crystal ball, but monetary policy used to be very predictable back then. It was much less so in the years that followed, and that predictability has recently returned.

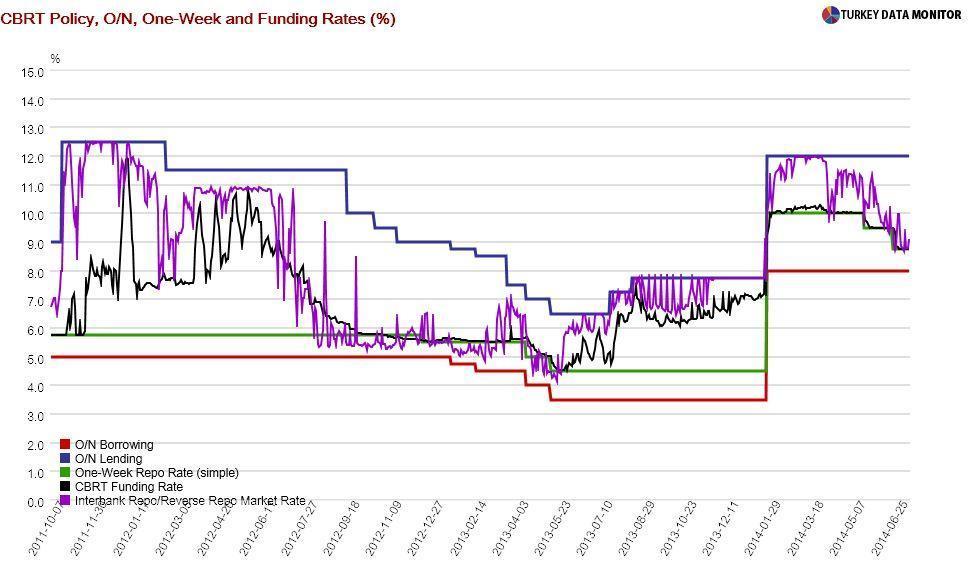

All of the 18 economists surveyed by AA Finans, state-owned Anadolu Agency’s knockoff Bloomberg/Reuters, expect a rate cut at the Central Bank’s rate-setting meeting on July 17, with most predicting that the Monetary Policy Committee (MPC) will lower the policy rate by 0.5 percentage points, from 8.75 to 8.25 percent.

This makes sense. At its latest MPC meeting on June 24, the Central Bank pledged to keep the yield curve, which shows returns on bonds with different maturities, flat until the inflation outlook improved. Its steepening since then has prompted Gov. Erdem Başçı to “redefine” the yield curve as the difference between the policy and benchmark two-year government bond rates.

The benchmark rate has fallen 0.3 percentage points since the last MPC meeting and at 8.30 percent, it is now 0.45 percentage points below the policy rate. So the Bank could justıfy a 0.5 percentage point cut. They will probably also refer to last week’s data, the weaker-than-expected industrial production and the decrease in the current account deficit, to rationalize their decision.

Will cuts continue over the coming months? Not according to markets. Participants in the Central Bank’s monthly expectations survey, which was released on July 11, expect the Bank to decrease its policy rate by 0.75 percentage points over the next three months and then pause. Financial markets are penciling in a slightly higher one percentage point cut during the same period.

It certainly won’t, but the Bank should hold rates, as the inflation outlook and latest global developments do not justify a rate cut at all. Inflation expectations, which are part of the same survey, worsened across the board. And tampering with a well-known financial term to justify lower rates is bound to hurt the Bank’s already-tarnished credibility. Not to mention that markets may try to pull policy rates to where they want- rather than the other way around.

Most importantly, rate cuts of this magnitude will not cut Prime Minister Recep Tayyip Erdoğan, who wants to see the policy rate at where it was before the emergency hike on Jan. 28, at 4.5 percent. Because of the active use of the interest rate corridor at the time, the effective rate hike was more like 3 percentage points. Another one percentage point cut would bring rates to more or less where they were in January. But I don’t think Erdoğan would be convinced.

The Central Bank should have taken the Erdoğan factor into consideration before implementing confusing and convoluted monetary policy tools. Now, they will have to deal with him when they stop cutting rates. As you make your bed, so must you lie in it!