Investors want to gobble up Turkey

I spent the first half of the week in London, invited by an investment bank to speak to their clients on the Turkish economy. I met with half a dozen or so investors on Tuesday.

I spent the first half of the week in London, invited by an investment bank to speak to their clients on the Turkish economy. I met with half a dozen or so investors on Tuesday.The title of my presentation, “Waiting for Godot: Investment Grade and the Turkish Economy,” became obsolete just as my plane landed in London, as Fitch upgraded Turkey to investment grade. As I had argued here almost a month ago, I was expecting the ratings agency to raise the country’s outlook rather than an outright upgrade to investment grade.

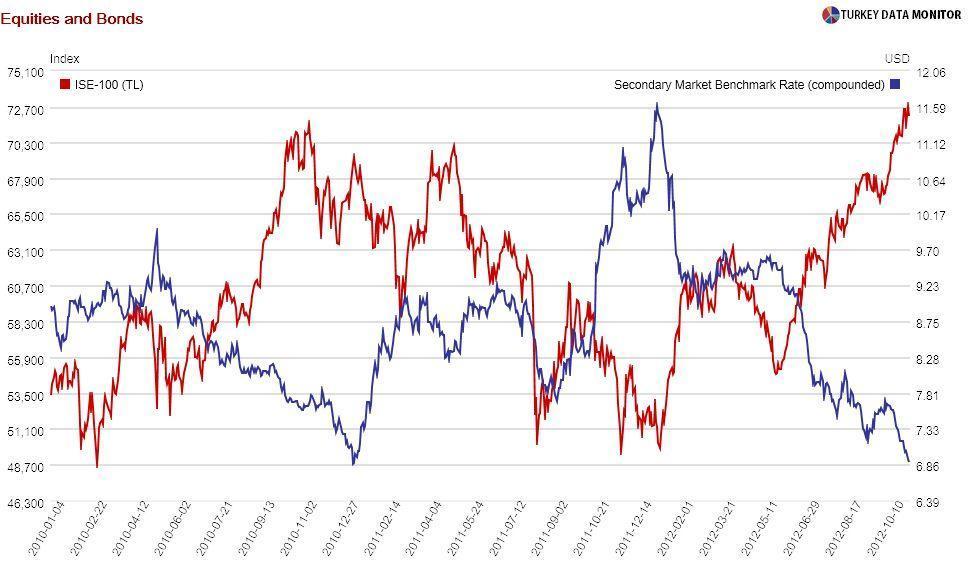

Unsurprisingly, Fitch’s action was one of the key topics of discussion. While some investors expected renewed interest in Turkish assets, others were more cautious. They argued that, with the Istanbul Stock Exchange at record levels and interest rates very low, equities and bonds did not have much room for improvement, and that there had already been solid flows to both since the beginning of the year.

Some also pointed out that Turkey needs an upgrade from at least one of the other two main rating agencies to be considered investment grade by many funds, including large institutional investors. While Standard & Poor’s rates Turkey two notches lower than investment grade, Moody’s is only one step below. But everyone was wondering how the Central Bank would respond if capital flows to the country were to increase.

I expect a repeat 2010-2011, when the Bank initiated its unconventional monetary policy with a wide interest corridor and used required reserve ratios to curb credit growth. At its regular meeting with investors on Wednesday, the Bank mentioned these and Reserve Option Coefficients while noting they would shun outright foreign currency purchases, as they are costly to sterilize.

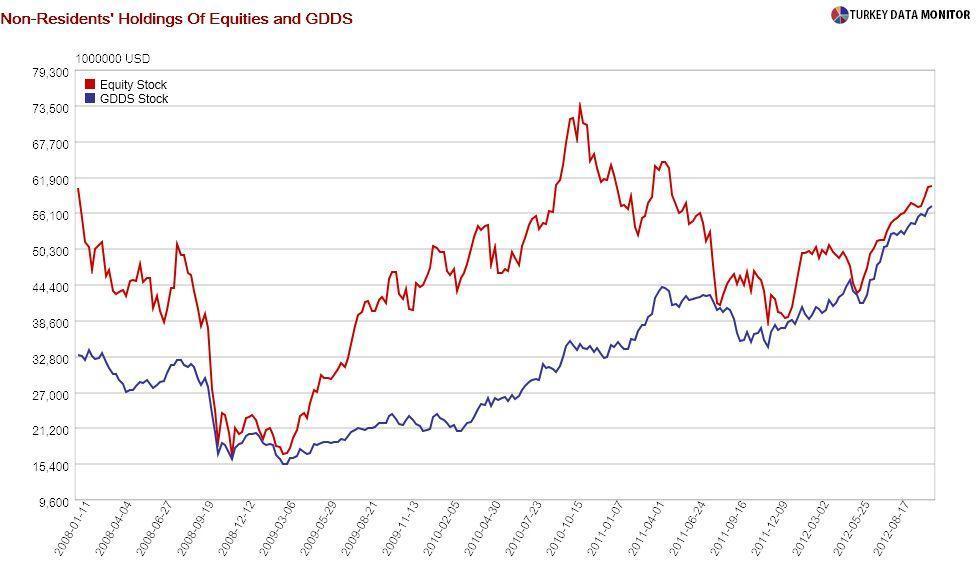

I found investors to be rather relaxed about the current account. While they agreed that a deficit of 7-7.5 percent of GDP looks very high, they also noted that the nominal amount of $60 billion this ratio corresponds to is peanuts for the Federal Reserve. They underlined the huge interest in emerging markets (EMs), as investors are chasing yield.

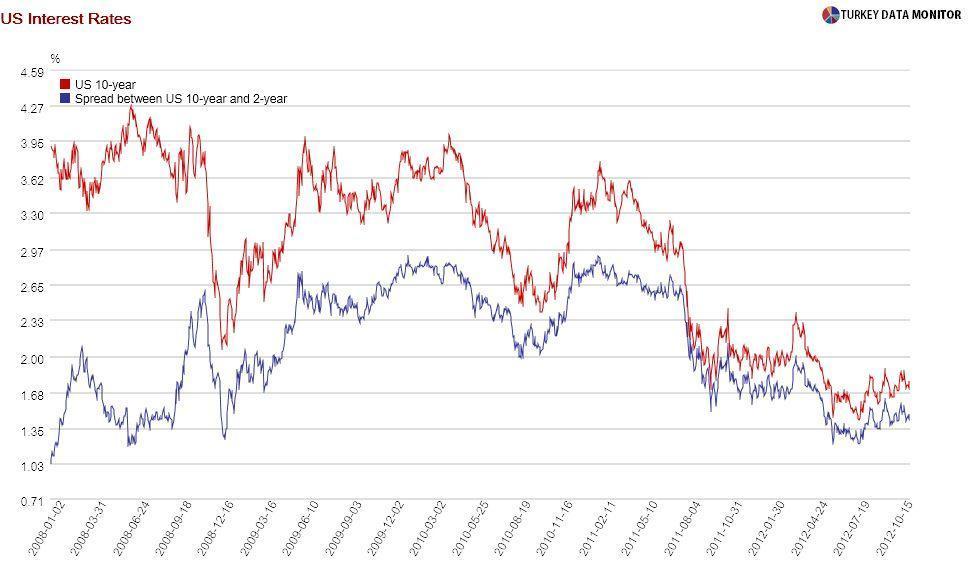

In this sense, a robust U.S. recovery and rising interest rates, which would put a stop to capital flows to EMs, were noted as the biggest risks facing the Turkish economy. Some said they would not be worried even then: Even if EMs faced a sudden stop, funds would be directed from peers to Turkey, as it is more beautiful, or at least less ugly, than they are.

Most investors agreed with my main scenario that growth would pick up during the remainder of the year and in 2013, driven mainly by consumer demand and on the back of loose monetary policy and fiscal spending ahead of the local and presidential elections. While everyone seemed to share my enthusiasm for equities sensitive to demand, such as retail, not all were as pessimistic as I am about banks.

But as I pointed out, given my forecasting track record, non-financials would probably underperform and banks over perform.