G-20 plan for investment targets faces stiff opposition

ISTANBUL-Reuters

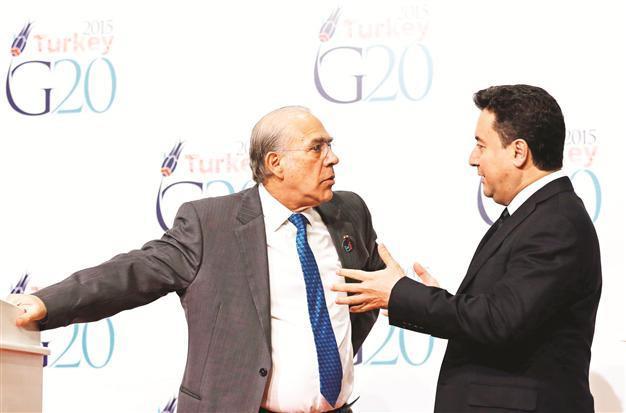

Turkey’s Deputy Prime Minister Ali Babacan (R) chats with OECD Secretary General Angel Gurria before a joint news conference during the G20 finance ministers and central bank governors meeting in Istanbul February 9, 2015. REUTERS Photo

Group of 20 finance officials look likely to reject a proposal to set countries specific investment targets to spur a global economy which looks increasingly reliant on the United States for growth.The meeting of finance ministers and central bankers in Istanbul comes as Greece casts a new shadow over Europe, cheap oil plays havoc with inflation and growth forecasts and a strengthening dollar threatens emerging economies.

Deputy Prime Minister Ali Babacan said Turkey, G20 chair for 2015, preferred to set binding national investment targets but it appeared to be struggling to win support.

“Would all international countries be committed? ... We don’t know yet,” Babacan said in a speech yesterday.

One G-20 source told Reuters the idea had already been taken off the table.

U.S. Treasury Secretary Jack Lew said last week the United States could not be “the sole engine of growth” and a senior U.S. official said Washington’s message would again be that Europe is not doing enough.

Germany, with its hefty current account surplus and a balanced budget, has come under pressure at successive G-20 meetings to spend more.

Berlin has rejected that suggestion in the past and is likely to argue that its rising domestic demand and plans to increase investment, largely through the private sector, shows it is doing what it can, according to European sources familiar with the G-20 agenda.

Its eurozone peers France and Italy have urged more investment in the struggling single currency bloc.

“We need to be bolder in Europe in terms of risk taking ... I hope that policy action will indeed facilitate stronger private sector investments, especially infrastructure investments,” Italian Economy Minister Pier Carlo Padoan told a financial gathering in Istanbul ahead of the G-20 meeting.

Leaders of the world’s top 20 economies agreed measures last year to raise their collective gross domestic product growth by an additional 2 percentage points over the next five years above the level projected in 2013.

The pledge, called the Brisbane Action Plan, entails about 1,000 commitments, which are now likely to be slimmed down to a more manageable number for each country to deliver on.

“Keep your word, or explain,” was how Babacan explained the strategy.

Coming good on those pledges could add more than $2 trillion to the global economy and create millions of new jobs over the next four years, International Monetary Fund chief Christine Lagarde said in a blog post.

Reform fatique

The Organization for Economic Cooperation and Development (OECD) said structural reforms had slowed over the past two years.

G-20 nations must focus on higher labor productivity and become more competitive and innovative if they want to boost growth, the OECD said in a report prepared for the meeting.

Bank of England Governor Mark Carney urged the G-20 to mount a “big push” to implement global regulatory reforms, fearing that governments may be tiring of non-stop rule-making since the financial crisis six years ago.

Carney was speaking as head of the Financial Stability Board which, since Lehman Brothers crashed in September 2008, has coordinated a raft of new banking and markets rules to make the financial system more resilient.

Meetings under shadows

The new Greek government’s refusal to extend an EU/IMF bailout and instead seek a new deal that ends austerity and restructures its debt will cast a long shadow at the Istanbul meeting.

Many of the main eurozone protagonists are here and the world is watching.

“There has to be compromise. It’s clear that Greece has got to be prepared to make some changes, and I think a wholesale repudiation of their debt is not on the cards,” Canadian Finance Minister Joe Oliver told Reuters in an interview. “But other countries, creditors will have to work with Greece to arrive at a compromise.

“I don’t think anybody wants Greece to leave the currency union.”