Eurozone, IMF clash over target times for Greek debt

BRUSSELS - Reuters

International Monetary Fund (IMF) Managing Director Christine Lagarde (L) talks with European Central Bank (ECB) President Mario Draghi at a eurogroup meeting in Brussels. The eurozone leaders and the IMF have different views on time granted to Greece to cut its debt, Lagarde says.

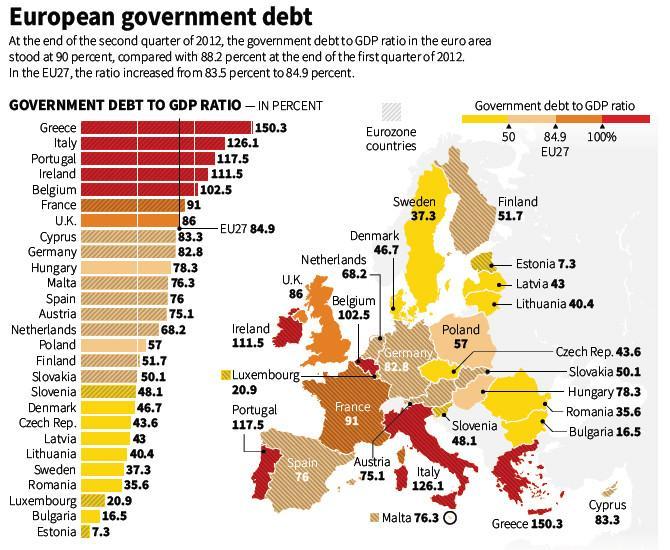

A clash between Greece’s international lenders over how the stricken country where the eurozone debt crisis began can bring its debts down to a sustainable level reignited fears yesterday that the crisis could flare up anew.Eurozone finance ministers suggested that Athens should be given until 2022 to lower its debt/GDP ratio to 120 percent but International Monetary Fund chief Christine Lagarde insisted the existing target of 2020 should remain.

“We clearly have different views. What matters at the end of the day is the sustainability of Greek debt so that country can be back on its feet,” Lagarde said late on Nov. 12, in an unusually public airing of disagreement.

Behind her sharp exchange with Eurogroup chairman Jean-Claude Juncker lies a rift over whether eurozone governments need to write off some of Greece’s debt to them to make it manageable. IMF officials have pressed for such a “haircut” while Germany, the biggest contributor to eurozone bailout funds, has vehemently rejected it as illegal.

‘Too ambitious’

German Finance Minister Wolfgang Schaeuble told reporters yesterday that the 2020 deadline was “a little too ambitious.”

“There’s a debate about a haircut for official creditors. On that I will say and most countries have said so in the past few weeks that that’s legally not possible,” he added.

Chancellor Angela Merkel has signaled she wants to keep Greece in the eurozone, but is determined to avoid losses for German taxpayers before a general election in September 2013.

With so much stake, diplomats remain confident that a deal will be done to release a 31.5 billion euros tranche of bailout money which Athens urgently requires to avert bankruptcy.

But it is a way off yet.

Financial markets, which have been calmed by the European Central Bank’s pledge to buy eurozone government bonds to shore up the currency bloc, took a dim view of the failure to agree.

The euro dipped to a two-month low against the dollar and safe-haven German Bund futures rose to two-month highs.

“There seems to be quite a big difference of opinion between the IMF and eurozone finance ministers ... but our view is still that Greece won’t leave the euro zone,” Rabobank rate strategist Lyn Graham-Taylor said.

Juncker, who heads the 17-nation group of eurozone finance ministers, said a further Eurogroup meeting would take place on Nov. 20 and officials said more negotiations could be required the week after that to nail down a new deal.

French Finance Minister Pierre Moscovici told reporters yesterday that bailout money should flow by the end of the month.

“Our objective is to reach an agreement in principle on Nov. 20 so that we can ... proceed to the disbursement of funds by the end of this month,” he said.

The delay leaves Athens scrambling to meet a 5 billion euro bond repayment deadline on Friday, but EU officials were confident that it would not default.

With Greece’s overall debt pile set to hit 190 percent of GDP next year, the IMF has set 120 percent as the target, saying that anything much above that is not sustainable given Greece’s low growth prospects and high external borrowing requirements.

“All avenues in order to reduce debt on Greece are being explored and will continue to be explored in the coming days,” Lagarde said.

TREASURY BILLS SAVE LIFE

ATHENS – The Associated Press

Greece has raised 4.06 billion euros ($5.15 billion) via the sale of short-term treasury bills, money that will help it make a crucial debt repayment on Nov. 16. Without the money raised yesterday, Greece would be staring at bankruptcy as the country’s international creditors have yet to sign off on the release of more bailout cash. Greece has to pay back 5 billion euros worth of bills that mature on Nov. 16.

Spanish consumer prices surge after tax boost

MADRID - Agence France-Presse

Spain’s decision to boost sales tax to curb a gaping public deficit sent consumer prices sharply higher in October, official data showed yesterday.

Consumer prices leapt 3.5 percent in October from a year earlier, the National Statistics Institute said in a report, confirming preliminary data released two weeks earlier.

The inflation rate was unchanged from September, when Prime Minister Mariano Rajoy’s government raised the top level of value-added tax to 21 percent from 18 percent.

Prices soared 10.5 percent for medicines after the introduction of patient contributions in July.

Teaching costs leapt 10.4 percent largely because of surging higher education fees.