Eastern Mediterranean gas: Why Turkey is key to its success

Soner KISTAK

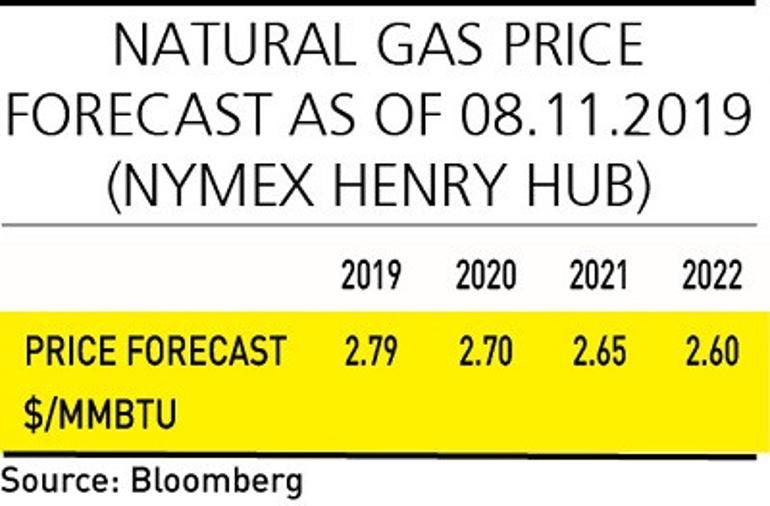

Worldwide demand for natural gas is growing, and there is currently no shortage of supply. Moreover, as alternative energy sources become more affordable, the price pressure and competition are likely to remain fierce. In fact, the natural gas price forecast for the next three years shows a flat trend with no significant upside potential. Since peaking at $13.40 around 2005, the price has dropped significantly below $3 in 2019. From a supply point of view, the gas price has been on a downtrend for a variety of reasons.

Contributing to the gas price decline, for example, are the U.S. shale gas revolution, the discovery of gas fields such as Galkynysh in Turkmenistan and Shah Deniz in Azerbaijan, to name a few; and more effective and efficient transport networks, such as upgraded U.S. major interstate pipelines Nord Stream, Blue Stream and Nabucco.

At the same time, important supply and demand happenings for Turkey have been taking place in the last decade. Turkey’s annual natural gas consumption increased from 35.3 billion cubic meters (bcm) in 2008 to 47.3 bcm in 2018. In addition, there have been gas discoveries in the eastern Mediterranean made by different stakeholders, and Turkey’s oil and gas pipeline has been substantially upgraded with a view toward full integration with European markets.

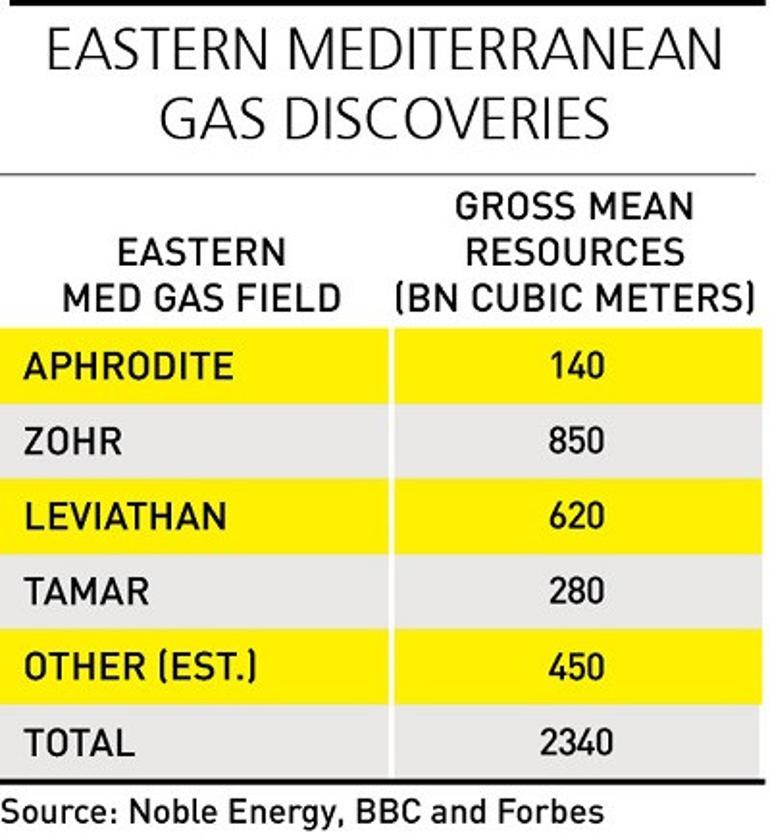

Although the relatively recent discoveries in the east Mediterranean are large for the region, they only represent a small amount globally. Even in the most optimistic scenario, the whole gas reserves in the region will only amount to a maximum of 2.5 percent of global reserves. Finding and developing gas is only a part of the challenge. Perhaps a more important challenge is to achieve a financially sound distribution and commercialization of the resource. In a context where gas prices will remain low for the near future, oil and gas companies will not be able to afford ambitious capital-intensive projects. For example, there are project-level discussions to have a 6 billion euro, 1,900-kilometer-long and up to 3-kilometer-deep pipeline from Israel to Italy via Greece. Such a project is not only technically difficult, but the capital costs will likely be much higher than the mentioned amount. Additionally, European oil companies would be reluctant to finance such large projects in the European Union’s current economic context of low growth. Even if they make it work technically, it is highly unlikely to result in competitive pricing with respect to Russian gas imports to Europe. Another proposal of constructing a Liquefied Natural Gas (LNG) facility would entail equally gigantic capital investments, and the product would not be able to compete with Iranian or Qatari exports in Asian destination markets.

Without getting into complex geopolitical considerations, the only financially-sound way for eastern Mediterranean gas to reach international markets is through Turkey. The Turkish option makes sense from several points of view.

Firstly, the closeness of Turkey’s Ceyhan port to east Mediterranean gas reserves is the most important factor. According to a feasibility study done by a private Turkish company back in 2013, the 450-kilometer pipeline from the Leviathan field to Ceyhan would cost around 2.3 billion euros - much cheaper than a 1,900-kilometer-long pipeline in the open sea.

Secondly, Turkey already has an established network of pipelines, which is well integrated with European markets. With 100 million euros in additional investment in mainland Turkey, east Mediterranean gas could easily flow into European markets.

Thirdly, Turkey remains one of the few countries with a sizeable industry in the region. The country would require increasing levels of natural gas imports in the region. Put differently, Turkey is not just a re-export market but also a gas consumption market. While Turkey enjoys good relations with its gas-supplying neighbors, it is also in Turkey’s interest to diversify its energy sources beyond Russia and Iran.

All these evaluations are based on rational financial considerations and do not necessarily consider current geopolitical matters such as the Cyprus issue, Turkey-Israel relations, etc. Moreover, recent U.S. and EU diplomatic interventions seem to overlook the potential of partnering with Turkey to commercialize the east Mediterranean gas. However, having an exclusionary approach that ignores this commercial perspective will not improve the situation.

Given that the whole region is going through economic difficulties and that, if history is any guide, commerce is a known and effective remedy for even the most difficult issues; a calm ring-fenced approach where divisive disagreements are put aside for the sake of this energy opportunity could create miracles for the east Mediterranean.